September 18, 2023 •Nathan Willis

Key Events: Strike

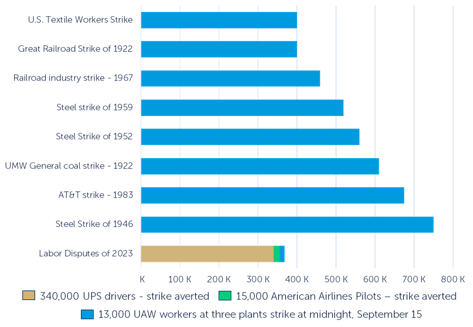

A targeted strike of 13,000 UAW workers affected Ford, Stellantis, and GM this week; the union is seeking to win back benefits forfeited during the ’08 financial crisis.

Inflation expectations continue to decline. The NY Fed 1-year expectations survey showed a decline to 3.6%, a drastic decline from the June 2022 peak of 6.8%.

As expected, the CPI data released on Wednesday ticked slightly higher based on increasing energy prices.

Market Review:Options expiration creates volatility

Stock options expiration led to increased volatility on Friday, and stocks gave up much, if not all, of the week’s gains.

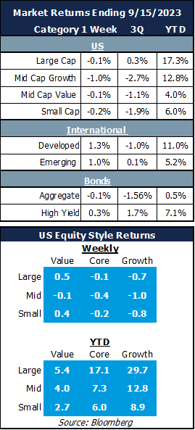

US stock performance this week was slightly negative, while international stocks held on to gains.

Outlook: Inflation and labor effect the economic picture

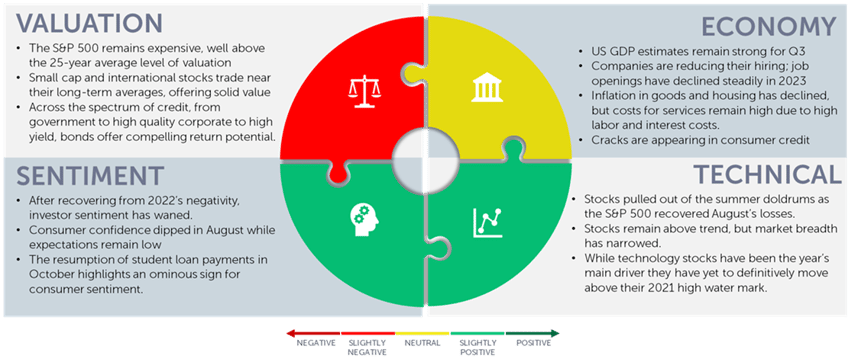

The headlines this week remind us of the tension in the economy: inflation is coming down, but labor costs have been going up for most sectors of the economy.

The fight to reduce inflation is likely to cause the economy to slow and unemployment to go higher. Given the prospect of a softening economy – and consumer – we must balance the risks in portfolios.

It is important to remember that attractive valuations (which can lower risk) can be found in many areas of the market, such as small cap, value and international stocks.

We encourage investors to remain broadly diversified in pursuit of gains.

The Biggest Strikes in US History[1]

Navigator Outlook: September 2023

This material is intended to be educational in nature,[2] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Statistica

[2] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggretate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00424