October 15, 2024 •Nathan Willis

Key Events: Stimulus hopes and inflation reminders

The Chinese government enacted further stimulus measures which were met with skepticism, seen as insufficient to resuscitate the economy or markets.

Consumer sentiment declined as Inflation pressures hit confidence; both consumer and producer prices, along with inflation expectations, came in hot this week while GDP estimates rose.

Market Review: Rethinking rate cuts

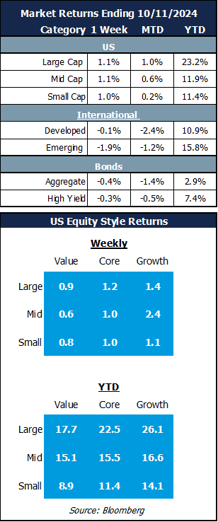

Bond returns were slightly negative this week; yields moved higher due to increased economic growth expectations and higher inflation data.

US Stocks turned in modest gains, but emerging markets dropped as Hong Kong and Chinese markets gave back a portion of their huge September gains.[1]

Outlook: Stronger economy, fewer rate cuts.

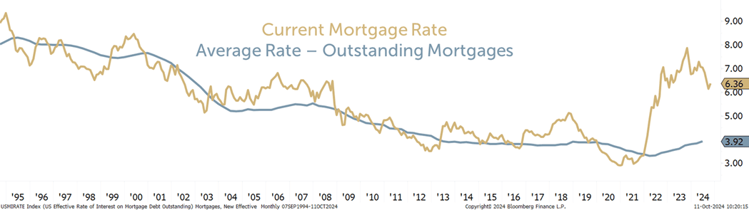

The chart below showing current rates and average rates for outstanding mortgages illustrates the tension between growth and inflation. New borrowers are spending far more than those with existing mortgages. Mortgage rates have risen since the Fed started lowering rates, suggesting the market is still worried about potential inflationary pressures.

Rising average interest costs will also put pressure on consumers and businesses. For now, though, economic growth is solid - the Atlanta Fed GDP Now model suggests 3.2% 3Q growth.

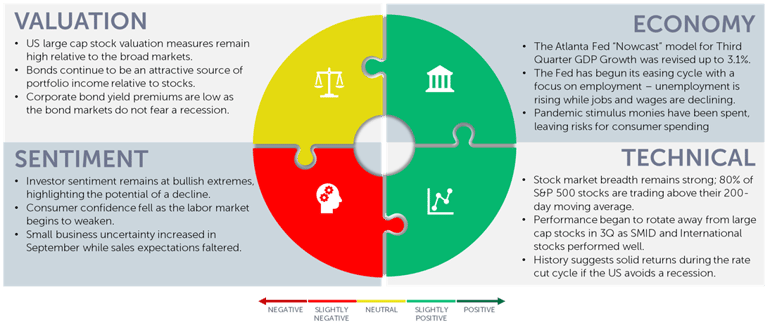

The tension between growth and inflation is likely to produce some volatility in the coming months. While current market expectations are for a soft landing, and our portfolios will benefit from solid growth, we are prepared for both inflation and potential slowdown.

Rate Cuts: Not moving the needle for mortgages [2]

Navigator Outlook: October 2024

This material is intended to be educational in nature,[3] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Bloomberg. CSI 3000 Index (China) and Hang Sen (Hong Kong) indices were up 21% and 18% in August but lost 3% and 6% this week.

[2] Source: Bureau of Economic Analysis, Bloomberg

[3] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggregate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00954