November 8, 2021 •OneAscent

Equity markets rallied again last week, as investors applauded a host of positive news throughout the week. The much-awaited Federal Reserve meeting wrapped up and while they shared plans to gradually taper their bond buying program between now and mid-2022, Fed President Jerome Powell indicated they are in no hurry to begin raising rates[1]. Markets reacted favorably to Powell’s patient messaging.

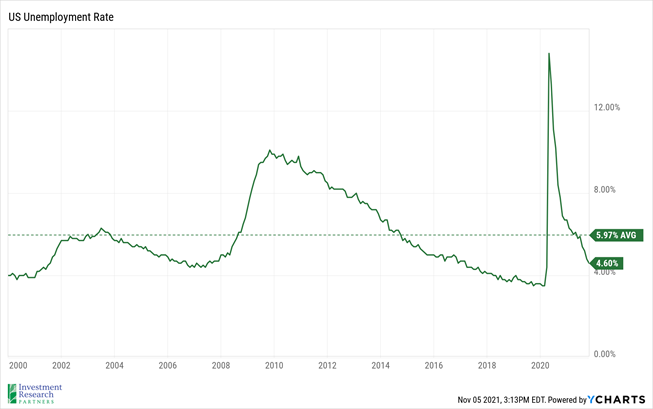

In addition, the US payroll report issued Friday surprised to the upside with 531,000 new jobs added last month, pushing the unemployment rate down to 4.6% (see graph below). That result easily bested economist estimates, which projected growth of 450,000 jobs[2]. Not surprisingly, nearly all major equity index posted positive returns for the week based on the news. The S&P 500 (a proxy for large-cap US stocks) was up 2% for the week and the MSCI ACWI index (a proxy for global large-cap stocks) climbed 1.6%[3].

Lastly, there was positive news on the pandemic front, as well. Pharmaceutical company Pfizer released clinical trial results for their Covid pill, reporting a reduction in deaths and hospitalizations in high-risk patients by 89%. The company plans to file for emergency FDA approval soon, and, if approved, the treatment “would be another tool in our toolbox to protect people”, stated President Joe Biden[4].

Prices & Interest Rates

| Representative Index | Current | Year-End 2020 |

|---|---|---|

| Crude Oil (US WTI) | $81.17 | $48.52 |

| Gold | $1,820 | $1,893 |

| US Dollar | 94.22 | 89.94 |

| 2 Year Treasury | 0.39% | 0.13% |

| 10 Year Treasury | 1.45% | 0.93% |

| 30 Year Treasury | 1.87% | 1.65% |

| Source: Morningstar, YCharts, and US Treasury as of November 6, 2021 |

Asset Class Returns

| Category | Representative Index | YTD 2021 | Full Year 2020 |

|---|---|---|---|

| Global Equity | MSCI All-Country World | 18.7% | 16.3% |

| Global Equity | MSCI All-Country World ESG Leaders | 21.6% | 16.0% |

| US Large Cap Equity | S&P 500 | 26.6% | 18.4% |

| US Large Cap Equity | Dow Jones Industrial Average | 20.5% | 9.7% |

| US Small Cap Equity | Russell 2000 | 24.4% | 20.0% |

| Foreign Developed Equity | MSCI EAFE | 12.8% | 7.8% |

| Emerging Market Equity | MSCI Emerging Markets | -0.3% | 18.3% |

| US Fixed Income | Bloomberg Barclays Municipal Bond | 1.0% | 5.2% |

| US Fixed Income | Bloomberg Barclays US Agg Bond | -1.0% | 7.5% |

| Global Fixed Income | Bloomberg Barclays Global Agg. Bond | -3.6% | 9.2% |

| Source: YCharts as of October 25, 2021 | |||

[1] Source: November 2021 Fed Interest Rate Decision: Federal Reserve Tapers, Holds Rates - Bloomberg

[2] Source: US Jobs Report October 2021: 531,000 Jobs Added, Unemployment Rate Drops to 4.6% - Bloomberg

[3] Source: YCharts

[4] Source: Pfizer (PFE) Covid-19 Pill Treatment Paxlovid 89% Effective on Hospitalization - Bloomberg

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.