November 13, 2023 •Nathan Willis

Key Events: $1 Trillion of interest

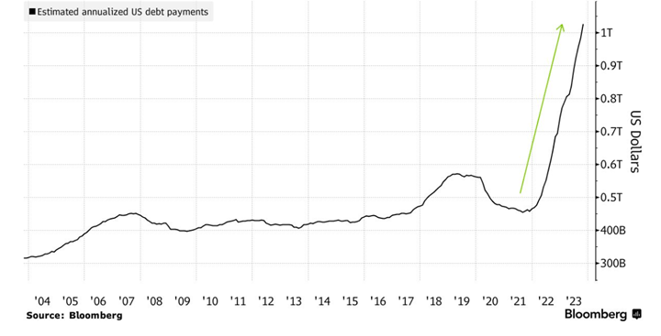

US debt costs $1 Trillion in interest,[1]a factor in Moody’s shift to negative outlook for US Government debt.[2]

Fed Governor Powell warned that he won’t hesitate to raise rates again if needed.

President Biden and China’s Xi Jinping are set to meet this week in an attempt to stabilize relations.

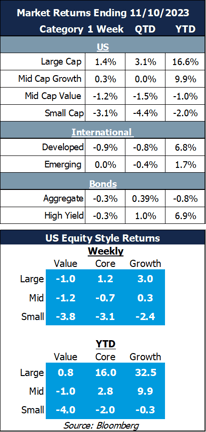

Market Review: Large Cap Stocks recover

Stock markets diverged this week: The S&P 500 recovered by over 1% but small cap stocks continued their declines: the Russell 2000 is negative for the year.

Bonds lost ground after Governor Powell’s comments.

Outlook: Earnings season recap and outlook

The third quarter’s earnings season turned out better than expected. With 92% of companies reporting, earnings have grown 4.1% over last year, up from an expected decline of -0.3% as of September 30.

The increase in earnings was broad – 9 of 12 sectors performed better than expected. Growth was, however, less than half of the five and ten-year average growth rate. For 2024, analysts are predicting 11.6% earnings growth on 5.5% revenue growth.[3]

We take (notoriously optimistic) analyst expectations with a grain of salt, as wage and interest rate pressures may counter high expectations, and high valuations reduce the margin of error. We are focused on maintaining exposure to areas of the stock market where valuations give us a greater margin of safety.

Cost of US debt Pile Surges[4]

Navigator Outlook: November 2023

This material is intended to be educational in nature,[5] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Bloomberg

[2] Source: Moody’s. Moody’s cited citied the US’ declining fiscal strength, higher rates, large deficits and political polarization in changing the outlook on United States’ ratings to negative.

[3] Source: FactSet

[4] Source: Bloomberg, US Treasury Data US Government’s Debt Interest Bill Soars Past $1 Trillion a Year - Bloomberg

[5] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggretate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00536