March 25, 2024 •Nathan Willis

Key Events: Chair Powell affirms the soft landing

A light economic news week was dominated by the Federal Reserve, which kept rates steady and suggested rate cuts are likely to begin this year.

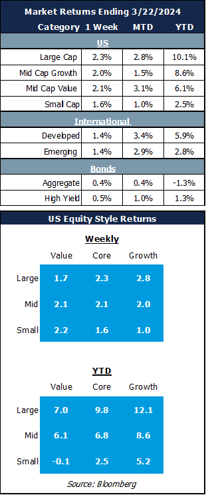

Market Review: Momentum continues

Markets are happily moving forward with the soft-landing narrative front and center: stocks rose across the board – Large, small and international all gained - and bonds stabilized.

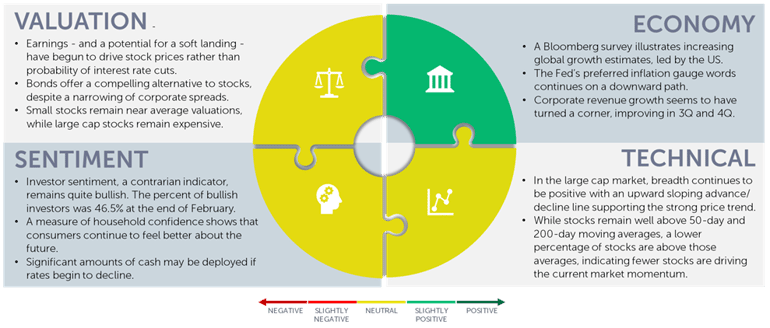

Outlook: What could go right

The market continues to expect a soft landing, and there is ample evidence to support this outlook:

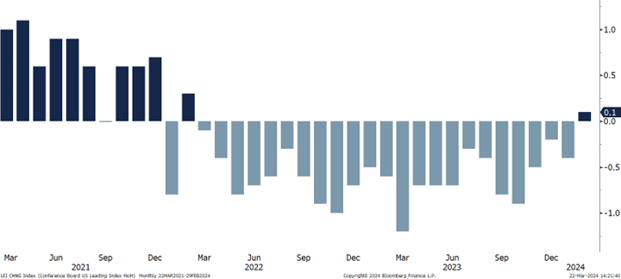

Leading indicators rose in February after 23 months of declines, ending the longest decline since the global financial crisis (see chart below).

- Earnings are projected to grow 10% in 2024[1]

- Inflation has subsided, allowing the Federal Reserve to expect rate cuts this year[2]

- Employment remains strong and consumer sentiment continues to recover from the Pandemic.

As a result, market returns have broadened. The equal-weighted S&P 500 index made an all-time high in early March after the cap-weighted index recovered its high in January. While small cap stocks, International Stocks and bonds remain well below their highs (14%, 8% and 10% respectively), they are making progress towards regaining their past highs.

Our portfolios are well positioned for a soft landing; Quality growth stocks and emerging markets will benefit from a strong economy and High Yield bonds will likely experience lower defaults. Use this link to sign up for our quarterly webinar to hear more Quarterly Market Update Registration.

Conference Board Index of Leading Economic Indicators - Monthly change [3]

Navigator Outlook: March 2024

This material is intended to be educational in nature,[4] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: FactSet – analysts project 5.1% revenue growth and 10.9% earnings growth for S&P 500 companies

[2] Source: Bureau of Labor Statistics – Core CPI has declined from a peak of 6.6% YOY (September 2022) to 3.8% in February

[3] Source: Conference Board, Bloomberg

[4] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggregate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00690