June 17, 2024 •Nathan Willis

Key Events: Processing the inflation data

The data this week presented conflicting signals from the Federal Reserve, consumer sentiment, and inflation:

Despite Wednesday’s lower consumer inflation report the Fed raised its inflation forecast and projected fewer rate cuts in 2024. Similarly, despite lower producer inflation reported on Thursday, a survey of consumer inflation expectations increased on Friday.[1]

Market Review: Confusion leads to volatility

This mixed messaging contributed to volatility. US large cap stocks, led by the tech sector, and emerging markets saw gains throughout the week. Conversely, small cap stocks reacted negatively to the economic uncertainty.

The lower inflation data offset concerns raised by the Fed and consumer surveys leading gains in the bond market.

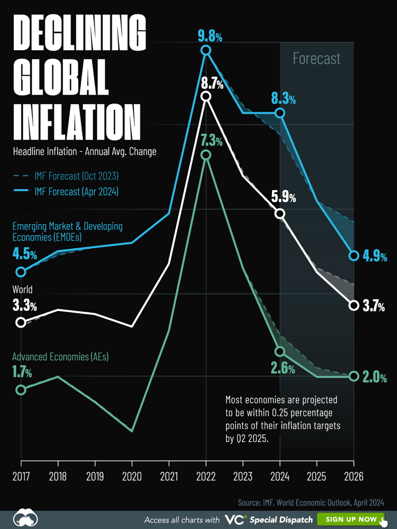

Outlook: Expectations and reality

The juxtaposition of lower inflation data against higher expectations is intriguing, as expectations often foreshadow actual inflation trends. Volatility is occurring as global inflation declines sharply from previous highs; predicting the decline accurately is challenging given the many factors beyond central banks' control. The Fed faces the delicate task of controlling inflation without pushing the economy into a recession.

A significant decrease in the University of Michigan consumer confidence survey this week reflects the worry that uncertainty may translate into economic weakness.

Given these uncertainties, rather than betting on a single outcome, we are positioning portfolios to benefit from a soft landing while preparing for potential scenarios of inflation or recession.

Forecasts for the decline of inflation [2]

Navigator Outlook: June 2024

This material is intended to be educational in nature,[3] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Bloomberg, University of Michigan – 1-year forward expectations were reported at 3.3%, above estimates of 3.2%.

[2] Source: Visual Capitalist Visualizing Global Inflation Forecasts (2024-2026) (visualcapitalist.com)

[3] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggregate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00810