July 31, 2023 •Nathan Willis

Key Events: Mission accomplished!! (??)

The Fed raised rates .25%, as expected, and guided that they were ‘data dependent’ about future moves. A trove of data releases increased the likelihood of a soft landing:

- Economic data continues to strengthen: The first estimate of the second quarter GDP growth was 2.4%, well above expectations of 1.8%, and Conference Board consumer confidence came in above expectations.

- Inflation cooled further, coming in below forecasts.

This “goldilocks” data – not too hot, not too cold, helped consumer sentiment continue its rebound.[1]

Market Review: Muted

Stocks’ reaction to the news was muted; The S&P 500 was up 1%, beaten only by emerging markets, up 2%.

Stronger growth prospects caused modest bond losses.

Outlook: Will the consumer drive the economy?

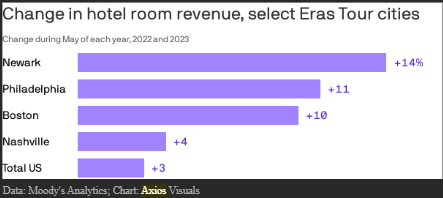

The economic influence of movie releases –Barbie, Mission Impossible and Oppenheimer – as well as concerts – the economic impact of Taylor Swift’s “Eras” tour is shown in the below graph – highlight a different aspect of ‘post-covid life: we are living it again.

This dynamic – along with AI hype – is behind the strong move up in equities. We acknowledge the strength, but also that Fed actions take quite some time to affect their intended economic consequence. We remain fully invested in a diversified portfolio while we monitor the performance of the economy.

Post Covid activity ramps up – Taylor Swift style[2]

Navigator Outlook: July 2023

This material is intended to be educational in nature,[3] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: University of Michigan Consumer Confidence Survey

[2] Source: Bloomberg

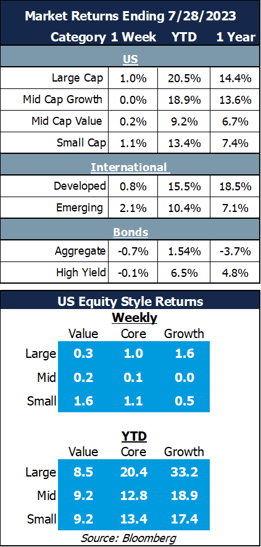

[3] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggretate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

{kind=link}

OAI00391