January 10, 2022 •OneAscent

A new year is underway, and it started off in a relatively inauspicious way for market participants. First the positive news – the US unemployment rate fell to below four percent in December and employee wages grew, as well.[1] The unemployment rate is now at its lowest point since February of 2020, before the Covid-19 pandemic overturned the global economy.[2]

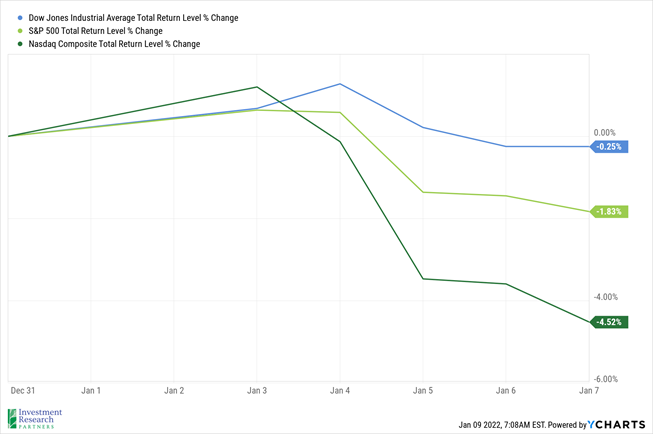

Somewhat counterintuitively, the improvement in labor has investors concerned that the US Federal Reserve will be forced to rein in inflation by raising rates more quickly than initially anticipated. That concern seemed to be justified with the release of the Fed’s December meeting minutes. Deemed as hawkish, the market dropped, leading to the worst first week of the year since 2016 for the S&P 500 index (a proxy for large cap US stocks).[3] Technology stocks, in general, fared even worse during the sell-off. The Nasdaq Composite, a technology-heavy US stock index, fell more than 4 percent for the week. By contrast, the Dow Jones Industrial Average, an index of large cap US companies with far less technology exposure, was nearly flat.

Prices & Interest Rates

| Representative Index | Current | Year-End 2021 |

|---|---|---|

| Crude Oil (US WTI) | $78.94 | $75.37 |

| Gold | $1,797 | $1,828 |

| US Dollar | 95.74 | 95.67 |

| 2 Year Treasury | 0.87% | 0.73% |

| 10 Year Treasury | 1.76% | 1.52% |

| 30 Year Treasury | 2.11% | 1.93% |

| Source: Morningstar, YCharts, and US Treasury as of January 10, 2022 |

Asset Class Returns

| Category | Representative Index | YTD 2022 | Full Year 2021 |

|---|---|---|---|

| Global Equity | MSCI All-Country World | -1.5% | 18.5% |

| Global Equity | MSCI All-Country World ESG Leaders | -2.0% | 20.8% |

| US Large Cap Equity | S&P 500 | -1.8% | 28.7% |

| US Large Cap Equity | Dow Jones Industrial Average | -0.3% | 21.0% |

| US Small Cap Equity | Russell 2000 | -2.9% | 14.8% |

| Foreign Developed Equity | MSCI EAFE | -0.3% | 11.3% |

| Emerging Market Equity | MSCI Emerging Markets | -0.5% | -2.5% |

| US Fixed Income | Bloomberg Barclays Municipal Bond | -0.7% | 1.5% |

| US Fixed Income | Bloomberg Barclays US Agg Bond | -1.5% | -1.5% |

| Global Fixed Income | Bloomberg Barclays Global Agg. Bond | -1.2% | -4.7% |

| Source: YCharts as of December 18, 2021 | |||

[1] Source: U.S. Jobs Report December 2021: 199,000 Added, Unemployment Rate Falls - Bloomberg

[2] Source: YCharts

[3] Source: Stock Market Today: Dow, S&P Live Updates for Jan. 7, 2022 - Bloomberg

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.