February 28, 2022 •OneAscent

The situation in Ukraine deteriorated rapidly this past week, moving quickly from a tense situation into a full-fledged Russian invasion that has put Ukraine’s 44 million people in jeopardy and shaken European security. Russia’s three-pronged attack has now closed in on Kyiv, the capital of Ukraine, however it remains under Ukrainian control at the time of this writing. The US and NATO allies have imposed a raft of sanctions against Russia, but the impact of most will be long-term in nature and it does not appear that they have made Russian President Putin second guess his decision to press forward thus far.[1]

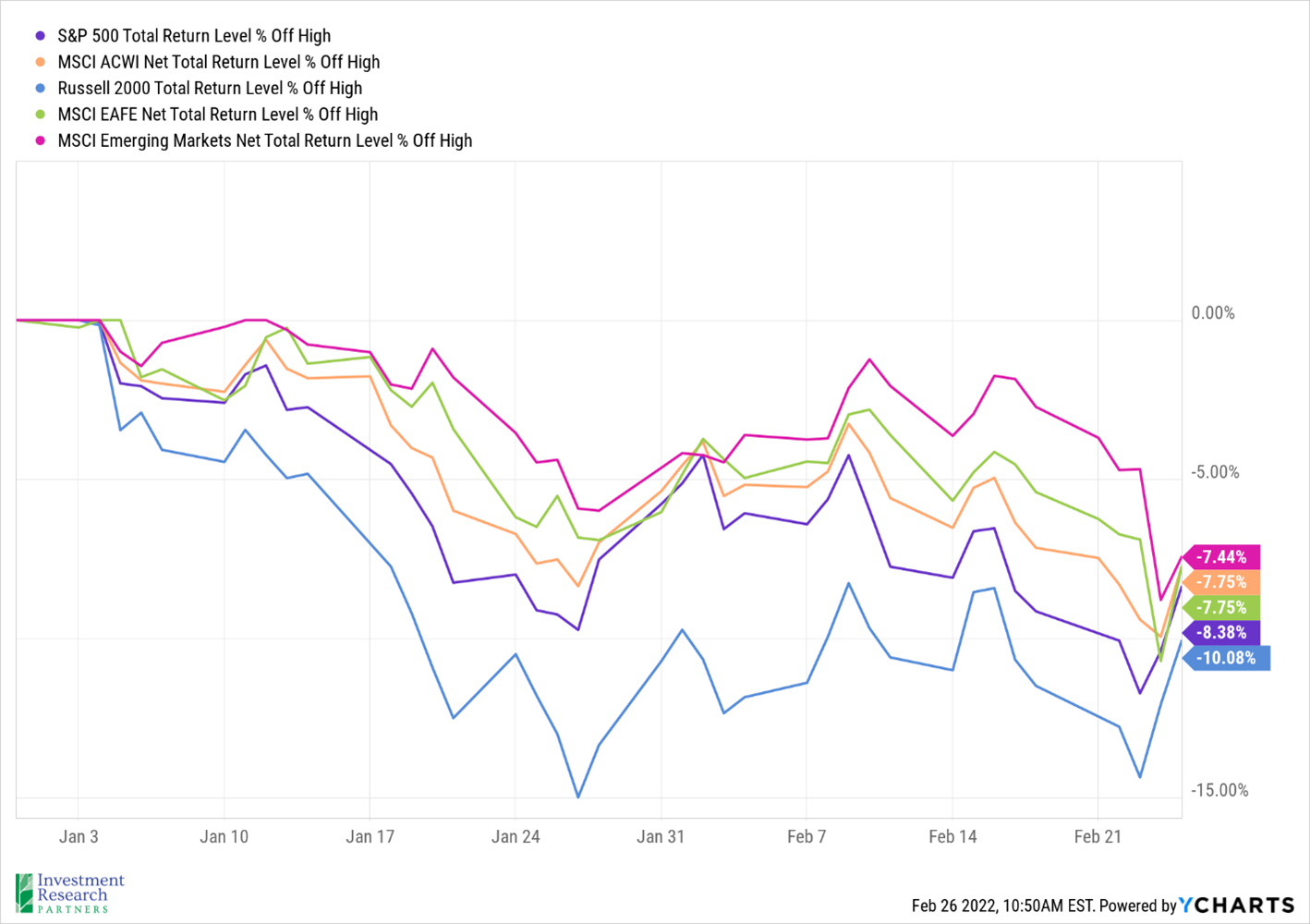

From a humanitarian perspective, the invasion represents a disaster for the Ukrainian people. An estimated 100,000 refugees have crossed into Poland so far and more are anticipated along European borders as the conflict continues.[2] From a market perspective, equity markets dropped significantly midweek as the invasion occurred but bounced back somewhat late in the week. The S&P 500 (a proxy for large-cap US stocks, purple line below) briefly dipped into correction territory (down ten percent or more from its recent high) but rebounded to end the week about flat. The MSCI ACWI index (a proxy for large-cap global stocks, orange line) ended the week down 0.6%, weighed down by foreign and emerging market stocks.

Prices & Interest Rates

| Representative Index | Current | Year-End 2021 |

|---|---|---|

| Crude Oil (US WTI) | $93.36 | $75.37 |

| Gold | $1,892 | $1,828 |

| US Dollar | 96.54 | 95.67 |

| 2 Year Treasury | 1.55% | 0.73% |

| 10 Year Treasury | 1.97% | 1.52% |

| 30 Year Treasury | 2.29% | 1.93% |

| Source: Morningstar, YCharts, and US Treasury as of February 26, 2022 |

Asset Class Returns

| Category | Representative Index | YTD 2022 | Full Year 2021 |

|---|---|---|---|

| Global Equity | MSCI All-Country World | -7.3% | 18.5% |

| Global Equity | MSCI All-Country World ESG Leaders | -8.4% | 20.8% |

| US Large Cap Equity | S&P 500 | -7.8% | 28.7% |

| US Large Cap Equity | Dow Jones Industrial Average | -6.0% | 21.0% |

| US Small Cap Equity | Russell 2000 | -9.0% | 14.8% |

| Foreign Developed Equity | MSCI EAFE | -6.6% | 11.3% |

| Emerging Market Equity | MSCI Emerging Markets | 4.8% | -2.5% |

| US Fixed Income | Bloomberg Barclays Municipal Bond | -3.2% | 1.5% |

| US Fixed Income | Bloomberg Barclays US Agg Bond | -4.0% | -1.5% |

| Global Fixed Income | Bloomberg Barclays Global Agg. Bond | -3.6% | -4.7% |

| Source: YCharts as of February 26, 2022 | |||

[1] Source: Russian forces pound Ukraine for third day, Kyiv still in Ukrainian hands | Reuters

[2] Source: Refugees flee Ukraine across EU borders as Russia renews assault | Reuters

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.