February 26, 2024 •Nathan Willis

Key Events: The soft landing begins to materialize

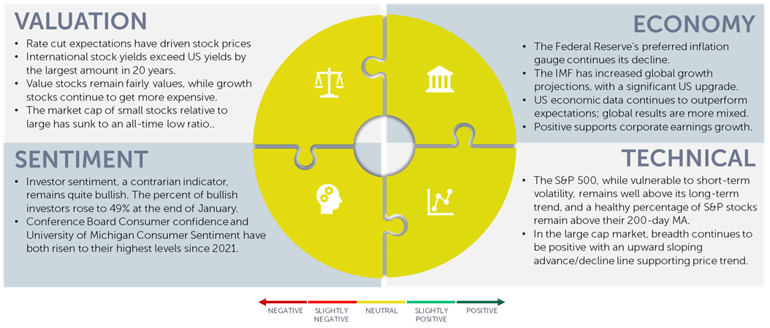

December’s Fed minutes illustrated that the board was surprised by US economic strength; consensus among Fed officials was that rates were likely to remain higher for longer. Economic data continues the positive trend the Fed saw in December.

Earnings data showed evidence of this strength as well; after declining for 2 years, S&P 500 revenue growth has increased for two quarters in a row[1], supporting the Fed’s soft-landing thesis.

Market Review: Processing profit growth

Markets quietly digested the prospect of a soft landing alongside earnings reports. Large cap stocks led the way on the heels of blowout Nvidia earnings.

Investment grade bonds were flat for the week while high yield gained as spreads reached their lowest levels since 2021, illustrating continued risk appetite.

Outlook: A new relationship with interest rates

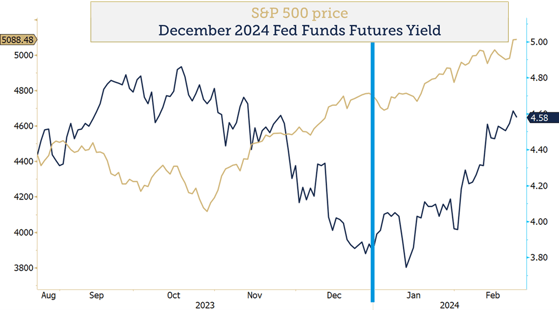

The chart below illustrates the changing relationship between stocks and rate cut expectations; in 2023 stocks were driven by expectations for rate cuts [1]. Fed Governor Powell’s dovish comments in October coincided with peak rates. Expectations for December Fed Funds dropped from 5% to below 4%, prompting stocks to rally through year-end.

We would cheer a soft landing, but we’re not banking on it. Our portfolios remain structured to benefit from strength but withstand potential adversity.

S&P 500 soars in 2024 despite expectations for higher interest rates[2]

Navigator Outlook: February 2024

This material is intended to be educational in nature,[2] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: FactSet Microsoft Word - Earnings_Insight_021624.docx (factset.com)

[2] Source: Bloomberg. Expectations for rate cuts illustrated by Fed Funds futures for December 2024, illustrating speculators’ estimates for interest rates at the end of 2024. A movements in Fed Funds Futures drove markets in 2023, a relationship which has not held so far during 2024..

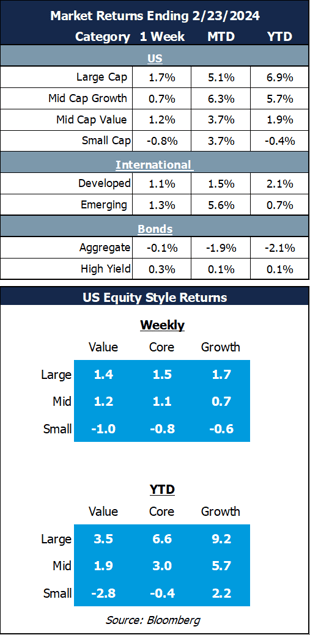

[3] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggregate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00652