December 5, 2022 •Nathan Willis

Key Events: The economy maintains strength while inflation moderates. The Fed plans to slow rate hikes

Key Events: The economy maintains strength while inflation moderates. The Fed plans to slow rate hikes

Several significant economic news items closed out November:

Third quarter GDP growth increased 2.9%, up from the first estimate of 2.6%. At the same time, inflation pressures eased slightly as October’s Core PCE slowed more than expected.

Fed Governor Powell struck a more moderate note in a Wednesday speech. The market seized on his dovish comments about slowing pace of rate hikes, despite indications from Mr. Powell that rates are still likely to remain higher for longer.

Market Review: Markets look to the Fed for direction

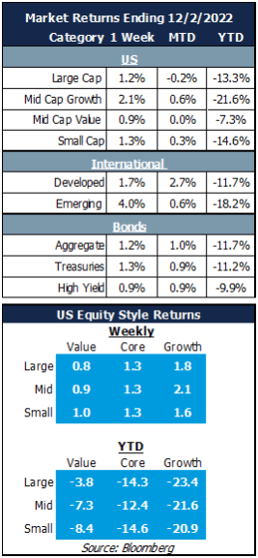

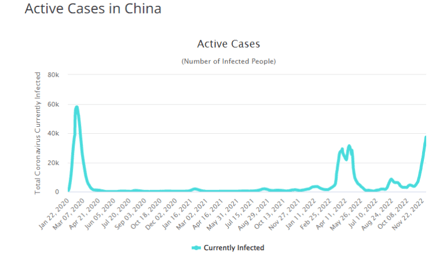

US markets reacted positively to Governor Powell’s speech, finishing off a strong month with modest gains. The S&P 500 finished the week up 1.2%, while international stocks posted stronger gains, benefitting from a weakening dollar and hopes that China will loosen its strict Covid-19 lockdown policies. These gains occurred despite a spike in Chinese Covid cases, as can be seen in this week’s chart. Emerging markets gained 4% for the week.

The broad bond market gained over 1% for the week, a positive reaction to the dovish rate hike outlook.

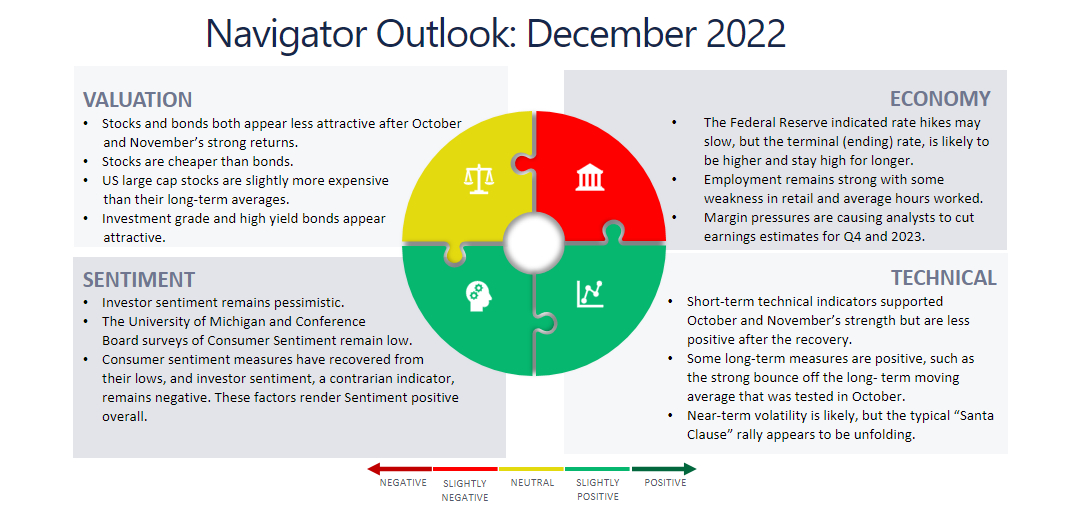

Outlook: Santa Claus rally?

As we move into December, investors begin to think about the holidays and look towards the new year. The markets often provide a “Santa Claus rally”; according to the Wall Street Journal the S&P 500 has risen 73% of all Decembers since 1928 and the average gain has been 1.4%. The fourth quarter has already given us strong stock market returns, bouncing solidly off of the October lows, so we may not expect such strong returns this year. Additionally, despite the market’s positive reaction to messaging from the Federal Reserve, Governor Powell has reiterated the Fed’s commitment to fighting inflation. This causes us to temper our expectations of a year-end rally. Given a high level of uncertainty, we remain disciplined and diversified.

Source: Worldometer China COVID - Coronavirus Statistics - Worldometer (worldometers.info)

Download PDF Version

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00085