December 27, 2021 •OneAscent

As we approach the beginning of a new year, it is only natural to reflect upon the year that was to remind ourselves how we arrived at this moment. In the first section of this update, we summarize how markets have reacted year-to-date. In the second section, we identify some themes and trends that developed throughout the year and contemplate how they may impact 2022.

Market Recap

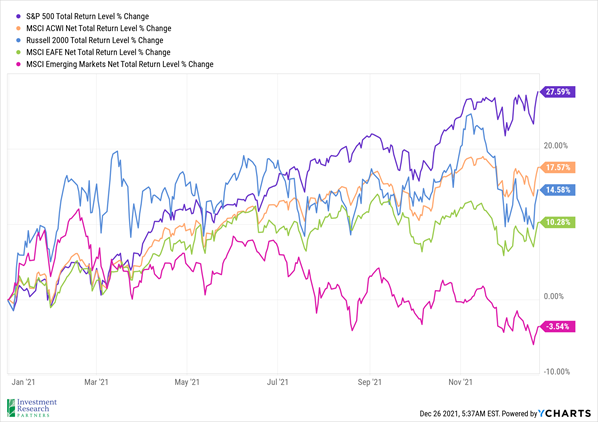

It has been a good year for risk assets, in general, as the rollout of vaccines and boosters created some sense of normalcy in the US and economic activity rebounded as the year progressed. Even as most equity markets experienced some volatility related to the omicron variant and inflation concerns the past few weeks, the S&P 500 (a proxy for large cap US stocks) is up over 27 percent year to date and the MSCI ACWI (a proxy for large cap global stocks) has advanced more than 17 percent so far this year (see the purple and orange lines below, respectively).

What may not be as obvious if you only follow a few stock indexes, is that not all parts of the market fared as well as the S&P 500. For example, small and mid-cap US stocks (Russell 2000 below) and foreign stocks (MSCI EAFE below) produced more modest gains. In addition, emerging market stocks (MSCI Emerging Markets below) have actually lost value so far in 2021.

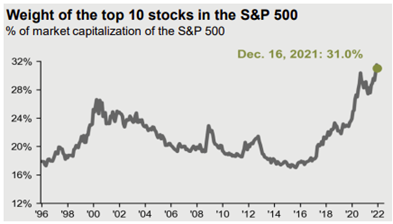

A big driver of the outperformance of the S&P 500 index over other stock indexes has been that market cap weighted models like the S&P have become increasingly top heavy. For example, the top ten stocks in the S&P 500 (i.e., Apple, Microsoft, Google, Amazon, etc.) now represent more than 30 percent of the index, a larger percentage than in more than twenty-five years (see graph to the right). Those ten stocks have, on average, outperformed the rest of the index year to date, creating a situation in which the concentration at the top has had an outsized impact on the overall index return.[1]

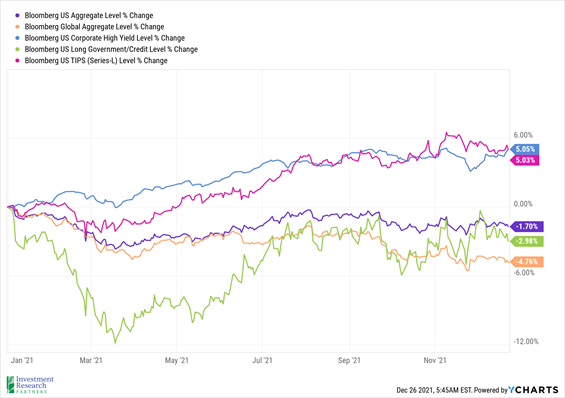

Unfortunately, the rising interest rate environment in 2021 created a very different result for most fixed income securities. For example, the Bloomberg US Aggregate Bond index (a proxy for US investment grade bonds) has lost 1.7% so far year to date (purple line below). Longer duration and global bonds have fared even worse (represented by the Bloomberg Long Government/Credit and US High Yield indexes, respectively). Two of the few relative bright spots in fixed income markets have been high yield and Treasury Inflation Protected bonds (TIPs), both up nearly five percent so far (represented by the blue and pink lines below, respectively).

For most investors, all of this adds up to another relatively good calendar year for diversified portfolios. Stocks, especially large cap US stocks, advanced at a pace that should have more than offset the bond market struggles in all but the most conservative portfolios. In general, the market has rewarded investors that did not lose their nerve in 2021 as we’ve continued to recover from the lows of the global pandemic.

2021 Themes: A Look Back

As mentioned earlier, a few themes seem to bubble to the top as we review all of the market commentary that we produced over the course 2021. While you can clearly see the fingerprints of each on markets this year, it will be interesting to see if they develop into longer-lasting themes or if they simply represented a moment in time.

Learning to Live with Covid

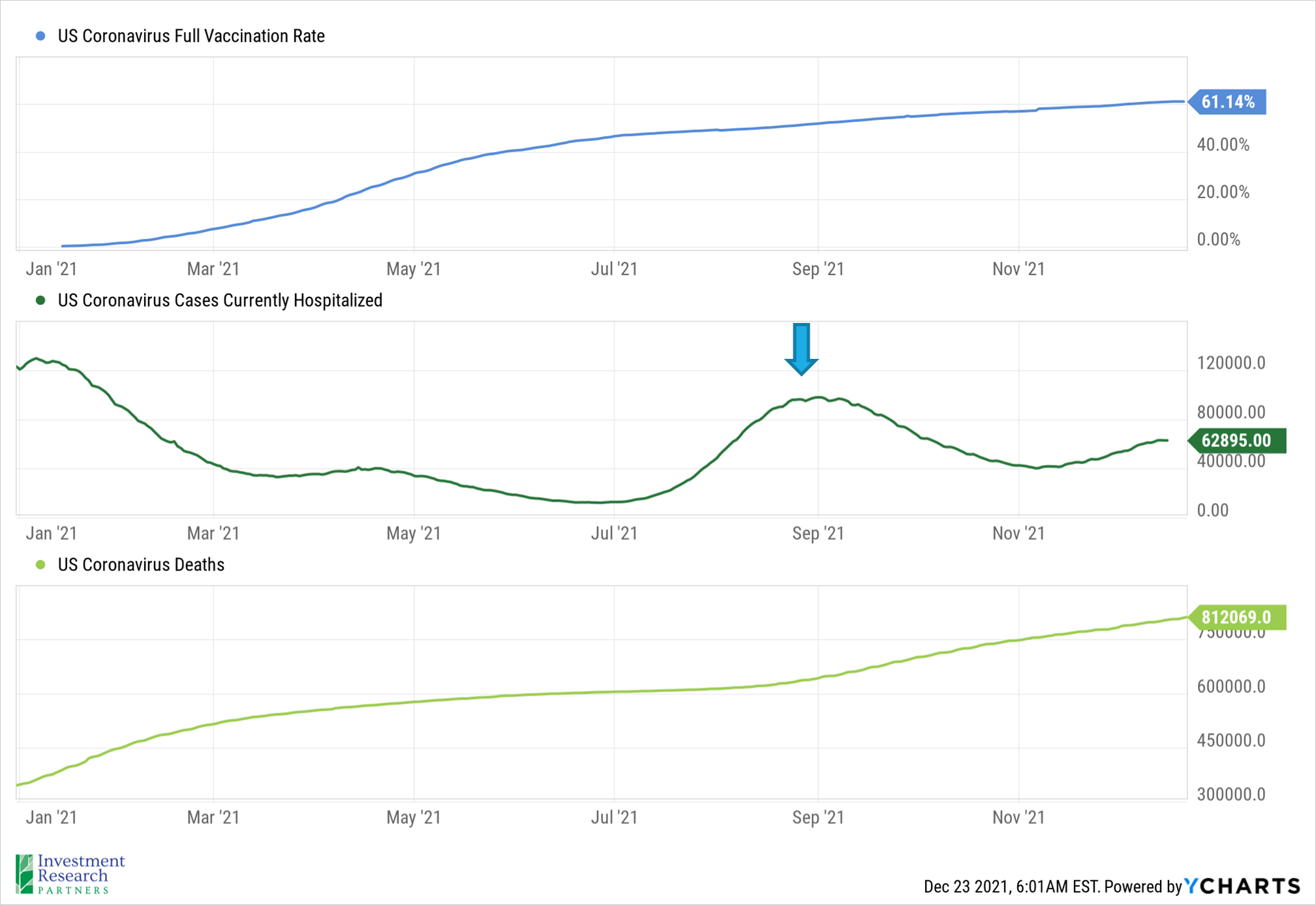

We would be remiss if we didn’t start with the pandemic. It is hard to imagine, but the vaccination rollout in most of the developed world was just picking up steam as we entered 2021. As things stand today, more than 60 percent of the US population is vaccinated and many have received boosters. Despite the progress, the delta variant created another wave of cases and deaths in August and September (see hospitalizations below), albeit slightly less severe than earlier in the year.

More recently, the CDC announced that omicron has now become the dominant variant in the country and its higher transmissibility is leading to a new wave of cases globally and prompting travel restrictions in Europe and flight cancelations in the US.[2] The positive news, at least so far, is that the new variant appears to be less deadly based on preliminary studies and both Pfizer and Merck just received FDA approval for their Covid-19 treatment pills.[3][4]

The world has been dealing with Covid for the better part of two years at this point and people and companies have been forced to adapt. Working from home, Zoom meetings, online classes, streaming movies, and home gyms are all much more prevalent than any of us could have imagined in 2019. Whether Covid remains with us in some form for another year or a decade or more is impossible to know, but we do believe that the lessons learned the past two years have made the economy more resilient to future surges.

Pop Culture and Crypto Make Waves

From meme stocks to non-fungible tokens, Robinhood to Dogecoin – the line between investing and speculation was questioned in 2021.[5] The combination of low-cost trading platforms like Robinhood, easy to use trading apps, and pandemic-related stimulus checks seemed to fuel an increase in online trading this year. That, coupled with online investing communities such as Reddit’s WallStreetBets and the rise (and fall) of various crypto assets, made for an environment in which speculation in assets not traditionally considered by Wall Street investment firms became more mainstream.

Whether this phenomenon is simply a function of the “risk-on” environment of 2021 or something longer lasting is difficult to say. The boom that some investors experienced this year may become a bust if the market’s appetite for risk dries up in the future. However, we do think it is important to question and consider the merits of new and emerging technologies, as some may become staples of the global economy in the future.

Inflation and the Shortage of Everything

The unique nature of the Covid-19 pandemic, essentially causing a global economic shutdown and subsequent restart, has brought with it unique challenges. One of the challenges apparent this year was that global supply chains struggled to ramp back up post-shutdown in order to keep up with demand. The result was the “shortage of everything”, as the inability to get key components drove up the price of both the components and the finished products that rely on them.

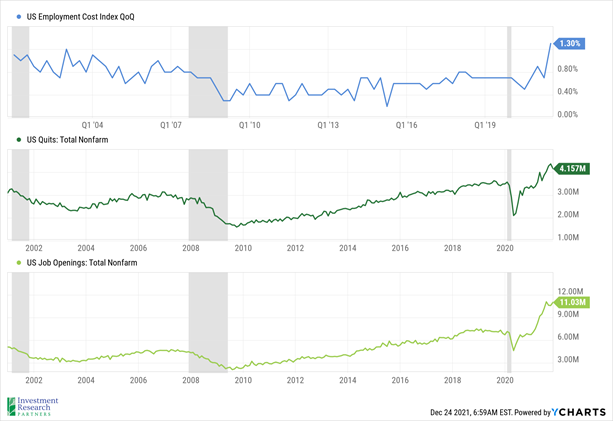

Another unique situation has been the shortage of workers this year. In what may be an underappreciated theme of the pandemic, workers deciding to leave their jobs voluntarily are near all-time highs (see dark green line below). The reasons may vary, from baby boomers deciding to retire with stock markets near record highs to parents leaving the work force to take care of children when schools went remote. However, the phenomenon is part of the reason that employers are having so much difficulty filling job openings (light green line, also near peak). The result – employers are paying more to fill open positions (blue line), adding to the inflationary environment.

These unique situations, along with the unprecedented level of monetary and fiscal stimulus, helped push the consumer price index (a measure of inflation) to 6.8 percent by year-end, the highest reading in 39 years.[6] The Federal Reserve (Fed) ended the year by acknowledging inflation as a major concern and indicating that it will unwind its bond-buying program sooner than previously communicated.[7] We will be watching inflation, and the Fed’s reaction to it, very closely in 2022. Whether the spike in inflation was a simply a 2021 phenomenon, or something longer lasting, has major implications for the economy and markets going forward.

Prices & Interest Rates

| Representative Index | Current | Year-End 2020 |

|---|---|---|

| Crude Oil (US WTI) | $73.76 | $48.52 |

| Gold | $1,810 | $1,893 |

| US Dollar | 96.07 | 89.94 |

| 2 Year Treasury | 0.71% | 0.13% |

| 10 Year Treasury | 1.50% | 0.93% |

| 30 Year Treasury | 1.91% | 1.65% |

| Source: Morningstar, YCharts, and US Treasury as of December 26, 2021 |

Asset Class Returns

| Category | Representative Index | YTD 2021 | Full Year 2020 |

|---|---|---|---|

| Global Equity | MSCI All-Country World | 17.6% | 16.3% |

| Global Equity | MSCI All-Country World ESG Leaders | 19.6% | 16.0% |

| US Large Cap Equity | S&P 500 | 27.6% | 18.4% |

| US Large Cap Equity | Dow Jones Industrial Average | 19.7% | 9.7% |

| US Small Cap Equity | Russell 2000 | 14.6% | 20.0% |

| Foreign Developed Equity | MSCI EAFE | 10.3% | 7.8% |

| Emerging Market Equity | MSCI Emerging Markets | -3.5% | 18.3% |

| US Fixed Income | Bloomberg Barclays Municipal Bond | 1.5% | 5.2% |

| US Fixed Income | Bloomberg Barclays US Agg Bond | -1.7% | 7.5% |

| Global Fixed Income | Bloomberg Barclays Global Agg. Bond | -4.8% | 9.2% |

| Source: YCharts as of December 26, 2021 | |||

[1] Source: YCharts

[2] Source: Omicron is now the dominant COVID variant in the U.S. : Coronavirus Updates : NPR

[3] Source: Omicron vs. Delta: Hospitalization Risk Is Far Lower With New Variant - Bloomberg

[4] Source: How to Get Pfizer Covid Pills? Biden Team Weighs Paxlovid Rationing Options - Bloomberg

[5] Source: 2021's Wild Year of Trading Stocks, NFTs and Crypto Changed Investing Forever - Bloomberg

[6] Source: YCharts

[7] Source: Powell Declares Inflation Big Threat as Fed Signals Rate Hikes - Bloomberg

Download PDF Version

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.