December 18, 2023 •Nathan Willis

Key Events: A Merry Christmas…

The Federal Reserve delivered Christmas cheer:

In his post-meeting press conference, Governor Powell said rate hikes “are not the base case anymore as it was 60, 90 days ago.”

On Friday, however, the New York Fed President said it would be “premature” to cut rates in March.

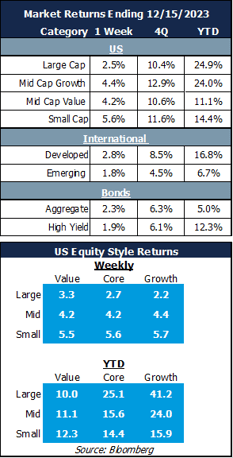

Market Review: Full speed ahead

The Market priced in a March rate cut, even though this view was tempered on Friday.

Bonds roared ahead, with the ten-year treasury yield dropping from 4.2% to 3.9% during the week, a move that caused the bond market to gain 2.3%.

Stocks rose across the board, with the biggest gains occurring in small caps as recessionary fears faded. International stocks gained modestly as well.

Outlook: …And a happy New Year!

Calming inflation data along with the Fed’s guidance affirmed Wall street’s soft landing viewpoint and, more importantly, expectations for gains in 2024.

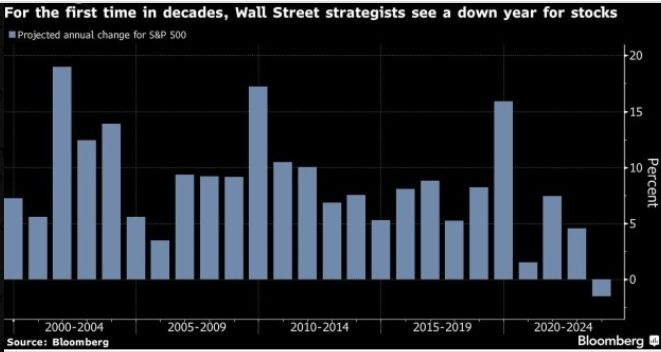

Ironically, 2023 was the first year in two decades that Wall Street actually predicted a down market. The S&P is up over 25% so far, but we don’t expect a repeat performance next year. We do expect that our diversified portfolio has a good chance of helping you move towards your goals. We will not publish next week, but we wish you a Merry Christmas and Happy New Year!

Wall Street Expectations were negative for 2023[1]

Navigator Outlook: December 2023

This material is intended to be educational in nature,[2] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Bloomberg

[2] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggregate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00562