December 11, 2023 •Nathan Willis

Key Events: Good news is bad news

Several pieces of economic data point to a strong jobs market, making it harder for the Fed to cut rates:

ISM services survey improved alongside last week’s manufacturing data.[1]

The November payroll report was strong with 3.7% unemployment.[2]

Market Review: A breather from the rally

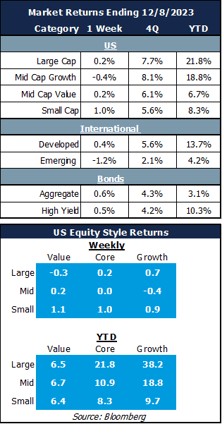

Stocks took a break after November’s stock surge, earning modest returns for the week. Smaller and more value-oriented stocks led the way.

Bonds gained again on reduced inflation fears.

Outlook: Expecting a soft landing

Economic data affirmed Wall street’s confidence in a soft landing. The market currently expects the Fed will start lowering rates in 2024, possibly in March.[3]

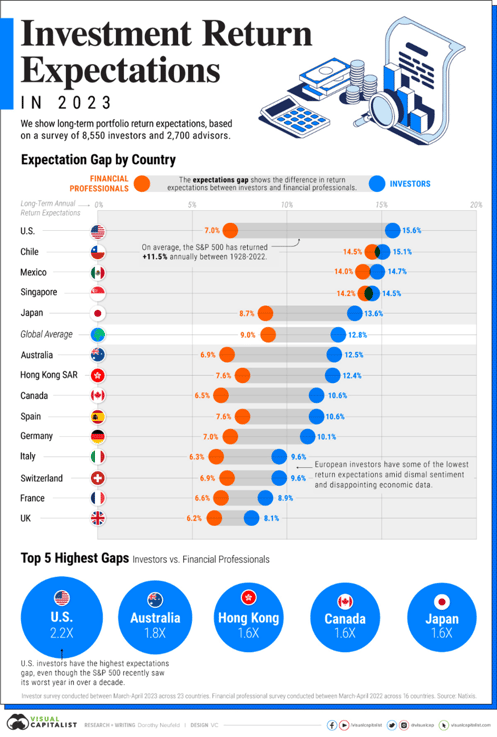

These lower rates may help propel stock returns that investors expect (see chart). We have lower expectations for the S&P 500. Our 10-year outlook is in the 7-8% range. Are we cynical or realistic? We don’t know.

But we do know that we are invested in a broad portfolio of stocks and bonds, many of which are relatively inexpensive and offer excellent return expectations. We will continue to espouse the benefits of diversification, a core pillar of our investment philosophy.

Great Expectations[4]

Navigator Outlook: December 2023

This material is intended to be educational in nature,[5] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Institute for Supply Management

[2] Source: Bureau of Labor Statistics

[3] Source: CME Group As of 12/8/2023, the market assigns a 45% chance of a rate cut in March, according to the CME Fed Watch tool

[4] Source: Visual Capitalist Visualizing Portfolio Return Expectations, by Country (visualcapitalist.com)

[5] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggregate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00553