August 12, 2024 •Nathan Willis

Key Events: The consequences of instability

Markets saw significant volatility as the Bank of Japan raised rates and the US jobs report increased recession worries, leading to the unwinding of leveraged trading strategies.

High valuations and market concentration made markets susceptible to this volatility spike. Geopolitical Instability also lies just below the surface as the middle east conflict risks breaking out into full-scale war.

Market Review: Volatility churns markets

This week the S&P 500 saw its largest YTD loss (Monday -3%) and gain (Thursday +2.3%) but ended the week flat.

The market spent the week caught between a growth scare, volatility shock, unwinding of leveraged trades and a mixed earnings season - the market needs strong earnings and an accommodative Fed to progress to the upside.

This uncertainty left small caps, international stocks and bonds all in the negative for the week.

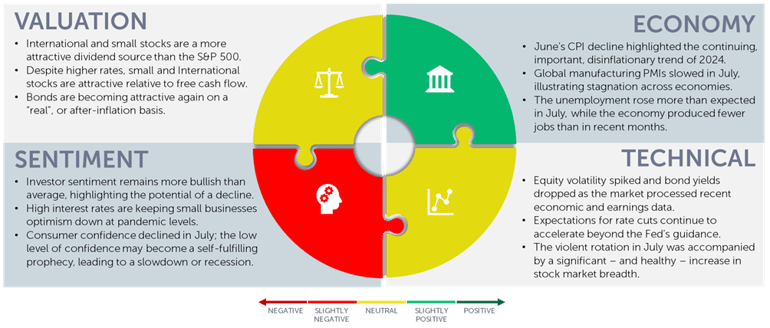

Outlook: Coping with instability

The broad losses across stocks and bonds serve as a reminder that things are, indeed, uncertain:

- The markets have avoided the recession narrative for some time, but now appear overly concerned.

- The AI narrative is waning as earnings season has caused a closer critique of some companies’ value propositions.

- Many factors have contributed to increased instability: An overly accommodative “post GFC” Fed, growth of passive investing, increased use of options strategies, and a reduction of security dealer inventories among others.

Not surprisingly, our advice is to do the thing that we have been doing all along – allocate to a diverse set of strategies, without placing too big of a bet on one outcome. We are in an environment that is very difficult to predict, so build a portfolio that won’t get hurt too much if the market goes against your view. We also advise investors to hold to our philosophy: values-aligned, long-term and globally diversified.

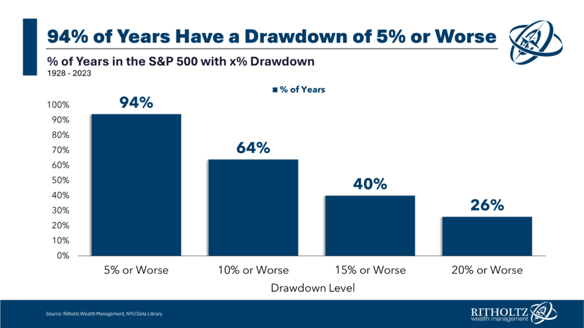

Short-term losses are normal[1]

Navigator Outlook: August 2024

This material is intended to be educational in nature,[2] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Rithotlz Wealth Management This is Normal - A Wealth of Common Sense

[2] Source: Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggregate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00913