June 22, 2021 •Will Sorrell

If you’ve glanced at the TV in the breakroom or perused the newspaper on a coffee table in the past month, you’ve likely seen the one word the entire financial world is debating right now—inflation. Inflation is typically one of those words you’d prefer to not see in the news. Like ‘taxes’ or ‘budget,’ inflation is necessary, but if it’s making headlines, there’s an inherent concern that your wallet will be impacted.

Before panicking or dismissing the issue, there are three simple questions that are wise to ask and answer.

1) What is inflation?

Inflation is ‘too many dollars chasing too few goods.’ It’s the rate at which the value of a currency declines as the prices of goods and services increase, or in other words, how quickly prices outpace your paycheck. It’s important to note that inflation is not inherently bad. Hyperinflation (when prices skyrocket out of control) and deflation (when price levels consistently fall) are the two sides of the economic enemy’s coin.

Last year, Federal Reserve Chairman Jerome Powell announced that the Fed will now target a 2 percent inflation average goal in the years ahead, compared to the previous 2 percent inflation fixed goal. This means that in the past, replacing your Nike workout shoes should have cost you 2 percent more in 2020 than in 2019. However, with a 2 percent inflation average target, some years the sparkling water might be 1 percent more expensive, but 3 percent more the next year.

2) Why is inflation so high right now?

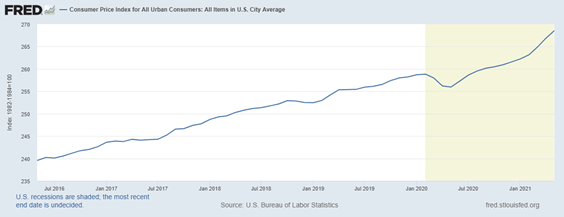

The chart below shows the Consumer Price Index’s year-over-year percentage change for the past five years. You can see that the inflation rate hovered mostly +/- 0.5 points of 2 percent until the pandemic began. In early 2020, price levels cratered, with inflation falling to 0.1 percent in May. The April 2021 inflation number was 4.2 percent, and it climbed to 5.0% in May, the highest levels since 2008. Is there cause for concern? Is this a blip, should you gear up for higher prices in the long-haul, or is hyperinflation around the corner?

Jon Hilsenrath from the Wall Street Journal provides a simple yet healthy framework for considering inflation today. Inflation can be caused by supply, demand, and stimulus, all of which are currently operating abnormally.

Supply and Demand.

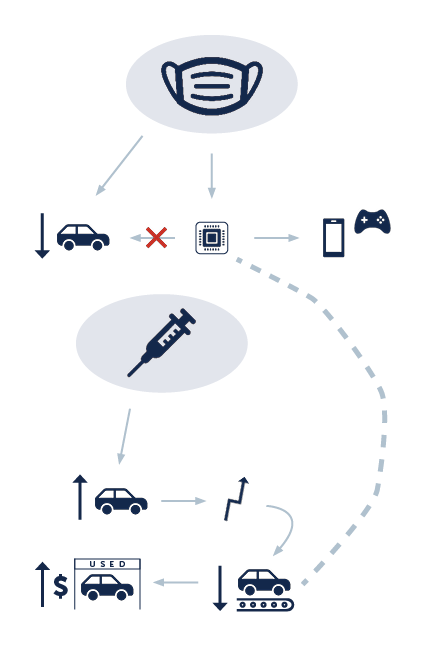

If you are in the market for a used vehicle right now, then you are experiencing inflation firsthand. The transportation industry accounted for more than half of the CPI increase in May, as used cars jumped an additional 7.3 percent last month after a 10 percent increase in April. The chart below breaks down the 0.6% month-over-month CPI increase from April to May 2021.![]()

The children’s classic If You Give a Mouse a Cookie explains this problem quite well.

If a global pandemic surges across the world, then people demand less cars. If people demand less cars, automakers produce less cars, so semiconductor companies make less computer chips for vehicles and more for quarantine essentials, like PlayStation 5s and iPhones.

If you give the world a vaccine, then people demand to come out of quarantine, maybe buy a car and finally take that cross-country trip they had to cancel in 2020. But if this demand increases more quickly than expected, like it has, then car manufacturers find themselves at the back of the line trying to secure chips to make cars. If Ford can’t make enough new Mustangs or F150s, then people will settle for used vehicles. If enough people want used vehicles, then the prices increase. If vehicle rental companies are also in the market since they sold off inventory to stay afloat in 2020, then prices skyrocket.

On top of Covid-19, add in a gargantuan boat crippling international supply chains, hackers holding oil and meat companies hostage, and lumbermill shutdowns increasing new home prices by $36,000 amidst a housing surge, and it’s been a very unfortunate 18 months.

In short, current supply and demand hiccups causing inflation are exactly that—hiccups. Half of US states are curtailing surplus unemployment benefits sooner than expected, and others are imposing stricter requirements. People are going back to work, demand will level out, and despite the pandemic forever altering our understanding of work and consumption, we will achieve a new normal.

Stimulus.

There’s an argument to be made that inflation should be high right now, because that’s a one-year percentage change number, and prices were falling amidst a nationwide shutdown in April and May of 2020. The real CPI number, not the year-over-year percentage change, looks much more normal. There was an expected dip in 2020 during the pandemic, and the graph has reverted to a mean of sorts.

Nevertheless, it’s worth asking, “What’s the long-term implication of all the stimulus money American individuals and businesses have received this past year?” No one can tell exactly how you saving, investing, or spending your $1,200 check signed by Uncle Sam will impact the economy a year from now. But there are a couple principles worth knowing as we monitor inflation rates going forward.

The Fed can finesse inflation rates in one of two ways: directly or indirectly. An example of direct influence would be the Paycheck Protection Program, doling out billions of dollars in forgivable loans to incentivize businesses to retain employees at the peak of Covid. An example of indirect influence would be changing interest rates—higher rates incentivize saving (taking dollars out of the economy) and lower rates incentivize borrowing (so you can buy an RV or renovate your ice cream shop).

Inflation is relatively elevated, yet the Fed is keeping rates low, contrary to what one would expect given that low rates can lead to more inflation. The Fed reasons that 1) the economy needs to ‘run hot’ right now so people will keep spending and working and emerging from quarantine, and 2) changing interest rates to change the inflation rate is like steering a barge—a slight adjustment can have a significant impact, but only down the road. Some argue that there’s no cause for concern, while others have little confidence in the Fed’s ability to act in the right time and manner when needed.

3) How can I protect myself from inflation?

To recap, inflation is elevated, but only compared to a prior pandemic year and a decade of relatively low inflation. The Fed walks a fine line between putting the economy fully back online and pumping too much money into the economy too quickly. In the short run, you should not be concerned. In the long run, you should have a plan ready for whatever life throws at you.

Are you prepared for the future? Here are a couple of questions to ask yourself to evaluate your portfolio.

- Are my investments primarily for distant future use, or am I about to begin spending my life savings in retirement?

- Is my portfolio diversified across multiple markets and asset classes in order to minimize inflation risk and maximize return potential?

- Are those managing my investments aware of the inflation question today? Are they strategizing for the future so that I am protected?

The OneAscent team remains diligent and watchful, ready to help you prepare for anything. If you’d like to discuss your plan, we’d love to hear from you!

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data. Please contact your Financial Advisor in order to complete an updated risk assessment to ensure that your investment allocation is appropriate.

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

Any charts, graphs, or visual aids presented herein are intended to demonstrate concepts more fully discussed in the text of this brochure, and which cannot be fully explained without the assistance of a professional from OneAscent. Readers should not in any way interpret these visual aids as a device with which to ascertain investment decisions or an investment approach. Only your professional adviser should interpret this information.