October 3, 2024 •Nathan Willis

September Review – The long-awaited rate cuts begin

The Fed finally began its long-awaited campaign of rate cuts in September! Why did they need to cut rates, and why did they need to do so now?

The two charts to the left illustrate the need [1]. The first chart shows that the pandemic stimulus provided a shot in the arm to consumers, shoring up their balance sheets during the pandemic.

The two charts to the left illustrate the need [1]. The first chart shows that the pandemic stimulus provided a shot in the arm to consumers, shoring up their balance sheets during the pandemic.

The bottom chart shows that US consumers spent through that money in early 2024. Consumers now must stand on their own, without the largesse of government stimulus packages.

Unfortunately, the labor market is now weakening – there’s no more free money to hire people and buy stuff. The Fed needs to support the economy because unemployment is beginning to rise and is able to do so because inflation has declined. This is a significant shift in the dual mandate of the Fed: the inflation fight is not the key issue anymore- it is time for the Fed to focus on maintaining full employment, stimulating the economy with rate cuts. We’ll talk about how this affects the outlook for the economy and markets, but first let’s review September’s returns.

Unfortunately, the labor market is now weakening – there’s no more free money to hire people and buy stuff. The Fed needs to support the economy because unemployment is beginning to rise and is able to do so because inflation has declined. This is a significant shift in the dual mandate of the Fed: the inflation fight is not the key issue anymore- it is time for the Fed to focus on maintaining full employment, stimulating the economy with rate cuts. We’ll talk about how this affects the outlook for the economy and markets, but first let’s review September’s returns.

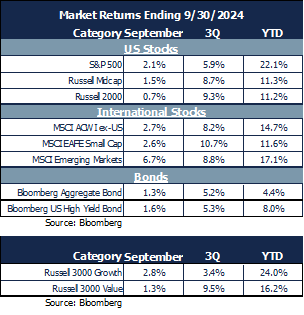

September Market Review

Stocks were positive despite September’s reputation as the worst month of the year:

- Large cap stocks gained 2.1% and are up 22% for the year.

- Small and midcaps gained, but less than large caps.

- Emerging Markets were the winner, as China enacted significant stimulus measures.

- Bonds performed well in response to increased expectations for rate cuts.

Stock sector movements reflected the rate cut campaign:

- Interest sensitive sectors – Real Estate, Utilities, and Financials – led the way as the market perceived that interest rate cuts are imminent. These sectors are expected to perform well during a period of declining rates.

- Technology and communications were the only sectors in the red for the month, giving up a small portion of their strong YTD gains.

- Energy was the only negative sector for the month, as oil prices continued to decline.

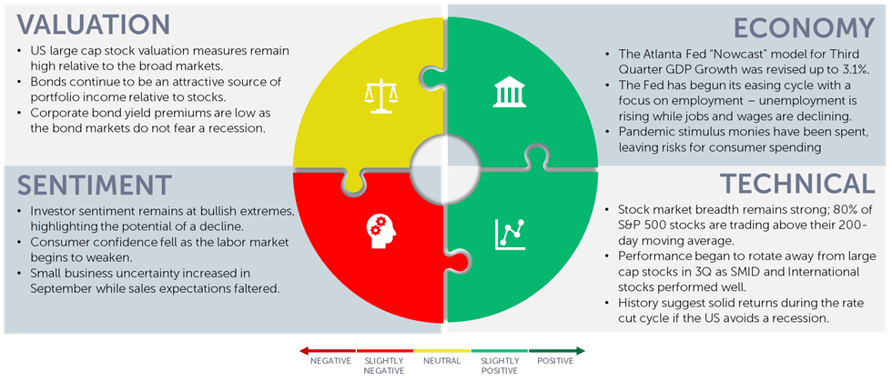

Our Navigator framework informs our outlook.

October 2024 Navigator Outlook

Economy: The Atlanta Fed “Nowcast” model for Third Quarter GDP Growth was revised up to 3.1%[2]. The Fed has begun its easing cycle with a focus on employment, which is rising while job openings and wages are declining. Pandemic stimulus monies have largely been spent, leaving consumers in a weaker position and highlighting the risks in an economy where consumer spending is a key driver.

Technicals: Stock market breadth remains strong; 80% of S&P 500 stocks are trading above their 200-day moving average[3], indicating solid momentum. Performance began to rotate away from large cap stocks in 3Q as SMID and International stocks performed well. History suggests solid returns during the rate cut cycle – as long as the US avoids a recession.

Sentiment: Investor sentiment remains at bullish extremes, highlighting the greater risk of short-term volatility. Consumer confidence fell, reflecting concerns over weakness in the labor market. Small business uncertainty increased in September while sales expectations faltered.

Valuation: US large cap stock valuation measures remain high relative to the broad markets. Bonds continue to be an attractive source of portfolio income relative to stocks. Corporate bond yield premiums are low as the bond markets do not fear a recession.

Outlook and Recommendations: watching the Fed and the earnings

Last month we noted that investor allocation to stocks is at an all-time high. Tech stocks have been the dominant force of wealth creation in recent years.

The charts to the right show that technology profit margins are as high [4] as they have ever been since the early 1990s! This has led to their highest valuations since the bursting of the dotcom bubble.  portfolios.

portfolios.

As valuations have grown, it becomes harder for these stocks continue their strong growth, and it becomes harder to meet investor expectations.

We have been looking for opportunities to invest beyond the large cap technology stocks by focusing on expectations for earnings growth.

Large cap earnings experienced slight declines in 2022-2023. The recovery in profits was driven by the technology sector but small cap stocks didn’t join the recovery.

This, however, is changing; large cap stocks are still growing, but small cap stocks are staging a strong recovery and are expected to grow significantly faster in 2025.[5]

Stock returns are beginning to reflect a tempering of expectations for large cap stocks.[6] While large cap stocks returned a respectable 5.9% for the quarter, technology stocks did not lead the way. small and mid-cap stocks returned 8.7% and non-US stocks 8.2%. Another indication of broadening stock market returns is the solid returns turned in by value stocks, up 9.4% for the quarter. We have talked for some time about the attractiveness of stock valuations outside of the S&P 500. Earnings are beginning to broaden, and returns – if the third quarter is the beginning of a trend – are beginning to broaden as well.

Valuations matter greatly for long-term returns. Small & Mid cap and international stocks, which trade at lower valuation levels, represent a compelling opportunity set for equity investors as these stocks return to earnings growth.

The Fed has shown its commitment to maintaining strong economic growth through its recently begun rate cutting campaign. This stimulus, along with the massive Fiscal deficits the government is running, are likely to support the economy – at least in the short term – despite being unhealthy for the long-term growth outlook.

Portfolio Positioning

We are positioned accordingly to take advantage of these opportunities:

- We remain globally diversified, with significant allocations to SMID and International stocks and lower allocations to large cap US stocks.

- Our portfolios are skewed towards quality stocks, likely to hold up better if the US economy experiences a recession.

- Our bond portfolios have a relatively neutral maturity profile and are positioned conservatively with lower exposure to high yield bonds.

- For those clients who prefer further diversification from both the stock and bond markets, we offer portfolios which utilize various hedged strategies to further manage short-term volatility.

Short-term volatility is a fact of investing life. While the market is doing well, we remind investors to remain disciplined and diversified in their portfolios. Trim risky positions and look for ways to shift your portfolio to areas with attractive growth potential.

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Federal Reserve Bank of San Francisco Pandemic-Era Excess Savings - San Francisco Fed (frbsf.org)

[2] Source: Federal Reserve Bank of Atlanta GDPNow - Federal Reserve Bank of Atlanta (atlantafed.org)

[3] Source: Bloomberg

[4] Source: Bloomberg Intelligence

[5] Source: Bloomberg

[6] Source: Bloomberg, OneAscent Investment Solutions – Data series includes: S&P 500 (S&P 500 index of large cap stocks), MSCI ACWI Ex-US (Morgan Stanley All Country World Ex USA index of non-US stocks), S&P 600 (S&P 600 index of small cap stocks)

OAI00948