November 6, 2023 •Nathan Willis

October Doldrums

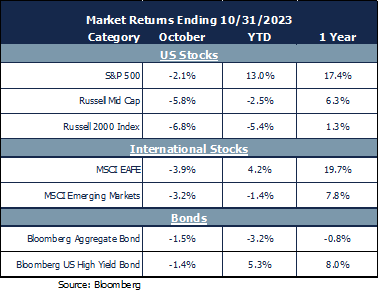

The three-month period from June through August saw the S&P 500 return 8.3%, a big departure from the expected ‘summer doldrums.’ However, September and October brought gloom to investors. The S&P 500 was down 7% in those two months, and small cap stocks lost 12%. Bonds joined the selloff.

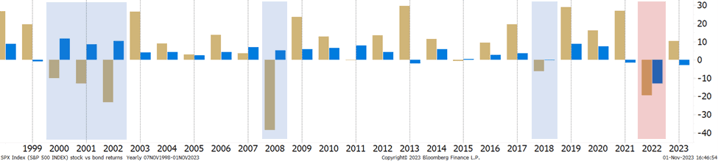

In 2022, for the first time in 25 years, calendar year losses in bonds accompanied calendar year losses in stocks. In fact, the increase in inflation caused bonds to sell off, which caused stocks to sell off. This phenomenon hasn’t happened in a generation and highlights the changing market dynamics.

Before we talk about what these changing dynamics mean for the future, let’s review October returns.

October Market Review

Stocks fell across the spectrum:

- Large US stocks ended down 2.1%, while small stocks and international stocks fell further.

- Bonds lost money as yields surged. At the same time, markets are processing the anticipated end of rate hikes.

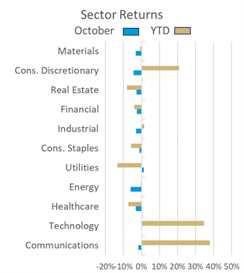

This may seem counterintuitive. If rate hikes are over, why are bond yields back up to highs last seen before the Global Financial Crisis? The answer lies in the economic support the Fed has provided since the GFC, which we will discuss further in our outlook. This dynamic has affected sector performance:

- Utilities were the only sector to make money in October. This is significant as they are the worst performer for the year-to-date period. Utilities are considered bond proxies, and the positive performance in October aligns with our view that bonds offer attractive returns going forward.

- Energy was the laggard in October after surging through the summer. Despite a spike mid-month on fears of a wider conflict in the Middle East, oil settled below $90.

Let’s review our Navigator framework to develop expectations for the rest of the year and 2024.

November 2023 Navigator Outlook

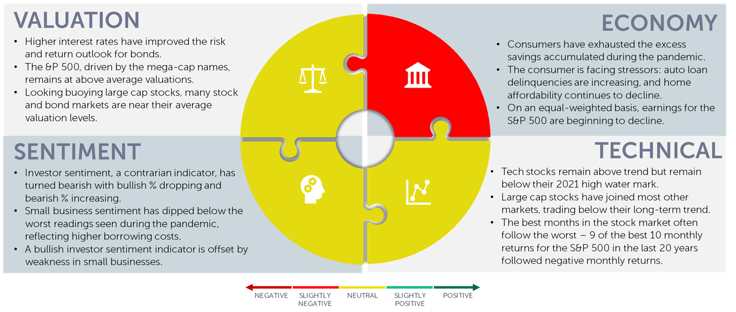

Economy: Growth was strong in the third quarter, but there are some clouds on the horizon. Consumers have burned through the pandemic stimulus measures. Weaknesses can be seen in the fact that auto loan delinquencies are increasing and the fact that home affordability has declined sharply; homebuyers need to earn $115,000 to afford a median-priced home in the US[1]. While mega-cap tech companies remain highly profitable, earnings are beginning to decline for the equal-weighted S&P index.

Technicals: The leaders of the market this year, technology stocks remain above trend but seek a catalyst to move above their 2021 highs. Large cap stocks have moved below their long-term trend, joining small and midcap stocks. However, strong months typically follow periods of weakness as we have experienced.

Sentiment: Investor sentiment has become quite bearish, which we view as positive. One significant area of negative sentiment is in small business owners, who are more negative than they were during the depths of the pandemic. Sentiment can become a self-fulfilling prophecy.

Valuation: Risk and reward dynamics have changed in the bond market Given the increase in interest rates, the upside – for a given decrease in interest rates – is far superior to the downside from a similar increase. While the S&P valuations is above averages, driven by the mega-cap technology names, many stock markets sport valuations much closer to their long-run averages.

Outlook and recommendations: wither diversification?

During recent down years for stocks (2000, 2001, 2002, 2008, and 2018) bonds made money–until 2022, that is. With virtually no inflation, bond yields were not a key driver of stock returns. Inflation reared its ugly head in 2022 and has changed the outlook for a balanced portfolio.

The potential for rates to remain high is weighing on stocks, and we must re-think the diversification benefits of bonds by considering times when inflation was a major factor in the economy. In the post WWII period, stocks had a higher correlation to bond yields as inflation was a key concern.[2]As inflation rose during the 1970s energy crisis, the S&P 500 experienced a bear market from 1973-1974.[3]

When the deflationary trends of technology and demographics kicked in during the 1980s, inflation became less of a concern; bonds offered effective diversification to stocks after the bursting of the tech bubble through 2020.

We need to think about bonds in our portfolios through an inflationary lens. We also need to consider the higher returns (yields) offered by bonds today—better than any time in the last 20 years. Two key conclusions present themselves:

- Bond Allocations may not provide as much diversification relative to stocks the way they have in the past 20 years. Bonds do offer solid returns even if rates don’t drop—better than they have for quite some time.

- Consider alternative investments alongside bonds. Strategies with low correlation to stocks and bonds may provide the diversification you need.

While the market dynamics are changing, we remain attentive to the opportunities available to seek solid returns while seeking out ways to manage risk. We remain ready and willing to take advantage of opportunities that market volatility may present.

[1] Source: Redfin A Homebuyer Needs to Earn $115,000 to Afford the Typical U.S. Home, More Than Ever Before (redfin.com)

[2] Source: Ned Davis Research

[3] Source: Aswoth Damodaran/NYU pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00526