December 5, 2023 •Nathan Willis

Bonds deliver an early Christmas present to the stock market

November highlighted the changing dynamics between the stock and bond markets, with implications for our 2024 outlook. A sharp decline in interest rates led to strong stock market gains in November. Rates dropped as economic data pointed to a slowing economy - just slow enough that the markets perceived the Federal Reserve was done raising rates and might even start cutting them in 2024. The Fed Funds futures market is pricing in rate cuts in 2024, beginning as early as January or March.[1]

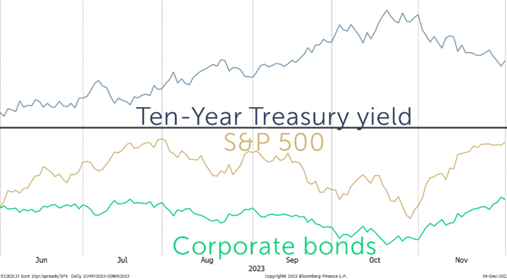

This chart shows that November brought a significant drop in treasury yields after a rise in the prior five months.

This led to a ‘risk-on’ environment, with both corporate bonds and US stocks recovering from October’s down month. In fact, many referred to November as the “everything rally,” with solid returns across the board.

Let’s review the month in detail before presenting our outlook and positioning.

November Market Review

Most markets had a solid rebound:

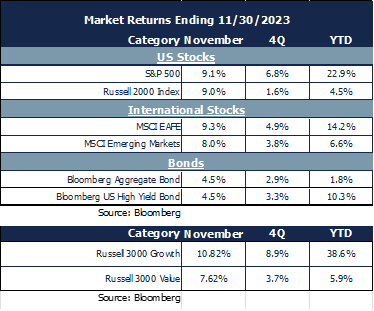

- Interest rates dropped across the yield curve – The ten-year treasury dropped from 4.9% to 4.3%, resulting in 4.5% positive returns for bonds.

- US stocks rose 9%, and international stocks did better. Emerging markets were the laggard, gaining “only” 8.3%.

- Growth stocks led the way during November and have gained significantly more than value stocks YTD.

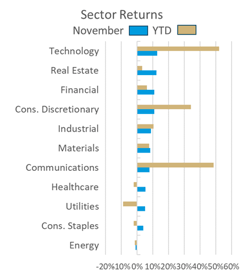

The movement of interest rates drove sector performance:

- Technology led the way, rising more than 12% as a decline in rates led to risk-taking in stocks. Technology stocks have gained more than 50% for the year.

- Real Estate and Financials, two interest-rate sensitive sectors, also gained more than 10% for the month on lower rates.

- Consumer discretionary stocks also performed well as hopes for an economic soft landing remain intact.

Our Navigator framework will inform expectations for December and 2024.

December 2023 Navigator Outlook

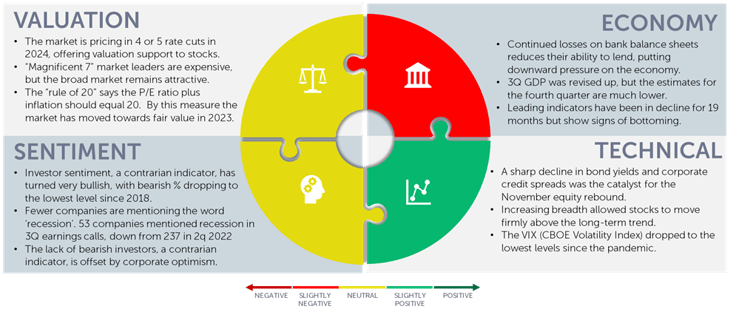

Economy: Losses continue to accumulate on bank balance sheets, which will likely lead to reduced lending activity. Growth was strong in the third quarter, but estimates are that fourth quarter growth will moderate. The Conference Board index of Leading Economic Indicators has fallen for 19 months but is showing signs of stabilization.

Technicals: A sharp decline in bond yields drove stock gains. This gain was characterized by strong breadth, as more stocks traded above trend. The VIX is signaling blue skies ahead, trading at its lowest level since the pandemic.

Sentiment: Investor sentiment has become quite bullish during November, which we view as a negative; the percentage of bearish investors has reached its lowest level since 2018. Companies are becoming more optimistic; 53 companies mentioned recession risk during third quarter earnings calls, down 78% from 237 companies during 2Q 2022.

Valuation: Bonds are providing valuation support for stocks; the bond market is pricing in 4 or even 5 rate cuts in 2024, starting as early as January. The “magnificent 7” market leaders are expensive on a Price to Earnings basis, but the broad market remains relatively attractive. The market has become cheaper on one interesting measure: the so-called ‘rule of 20,’ which suggests the stock market P/E ratio plus inflation should equal 20, indicates that stocks have been moving closer to fair value.

Outlook and Recommendations: A soft landing in 2024?

The markets went on a tear during November because investors began to price in a so-called ‘soft landing,’ which means achieving the Feds’ goal of price stability (inflation at their long-term target) and full employment. While a soft landing may happen, it has only happened once.[2]There are several data points we have discussed recently which argue against a soft landing:

- Leading indicators have declined to recessionary levels.

- Bank lending has declined, indicating corporate activity is likely to slow.

- Mortgage costs have become a greater and greater share of consumer’s wallets, reducing spending power.

- US Federal Debt service has grown to such a level that it may crowd out other borrowing, leading to higher interest rates for all borrowers.

- Analysts have reduced fourth quarter 2022 earnings estimates by 5% during October and November.[3]

This is not a comprehensive list, but it begs the question of how best to prepare for 2024 in case Wall Street is wrong and the soft landing turns into a recession. Our answer is relatively straightforward and consistent with our philosophy:

- While Bond Allocations may not provide as much diversification as they have in the past, they offer attractive yields and may perform better than stocks during a potential recession.

- Consider alternative investments alongside bonds. Strategies with low correlation to stocks and bonds may provide the diversification you need.

- Diversify your stock portfolio. We see attractive opportunities in International, Small, and Mid-cap stocks, as well as other strategies. Diversification away from the mega-cap drivers of the stock market makes sense.

Finally, and as always, stick with your plan. If you are worried, consult with your advisors to make sure you are on track. We wish you a wonderful Christmas season and a happy 2024.

[1] Source: CME Group Fedwatch tool CME FedWatch Tool - CME Group

[2] Source: “Landings, Soft and Hard: The Federal Reserve, 1965–2022”, Alan Blinder, Journal of Economic Perspectives. https://www.aeaweb.org/articles?id=10.1257/jep.37.1.101. St. Louis Fed What a Soft Landing for the Economy Means and What to Look At (stlouisfed.org) Wall Street Journal The Elusive Soft Landing Is Coming Into View - WSJ

[3] Source: FactSet. Analysts estimates drop, on average, 2.9% during the first two months of a quarter. Analysts Making Larger Cuts Than Average to EPS Estimates for S&P 500 Companies for Q4 (factset.com)

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00550