March 4, 2024 •Nathan Willis

February review –The soft landing takes the stage

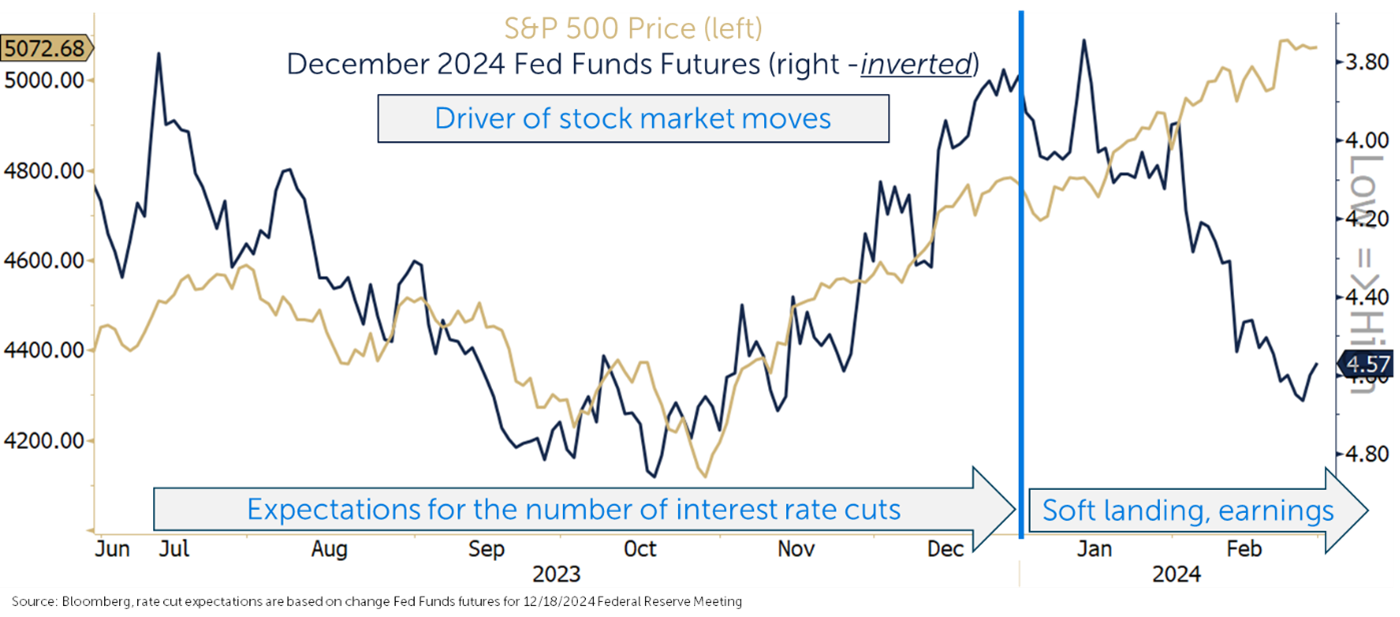

For much of 2023 the market focused on the Fed. The end of rate cuts dominated the first half of the year, and the market moved down(3Q) or up (4Q) based on the market’s view of when, and by how much, the Fed would cut rates in 2024.

A new narrative came into focus during February: The market now believes the Fed will engineer a soft landing. This shift from 2023 market movements can be seen in the chart as, in contrast to 2023, expectations for rate cuts have fallen while stock returns (S&P 500 at least) have been strong.

February Market Review

Markets digested the growing potential of a soft landing:

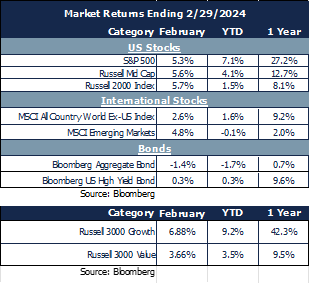

- Interest rates rose, causing losses for the broad bond market. High Yield bonds managed to remain slightly positive.

- Large stocks rose 4.9%. The market broadened, though, as small caps outperformed with a gain of 5.7%.

- Growth continued to outperform value.

- International stocks rose, but less than US stocks. Emerging markets bounced back as risk appetite took hold.

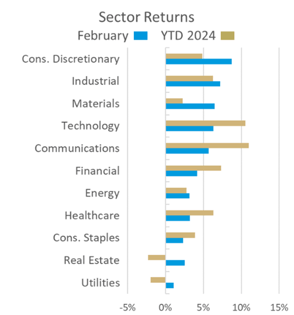

February sector movements reflected the soft landing narrative:

- Consumer discretionary, industrials and materials were the top three sectors as growth accelerated.

- Real Estate and Utilities dropped as bond yields rose.

- Overall, growth sectors significantly outperformed value sectors for February, as they did in January.

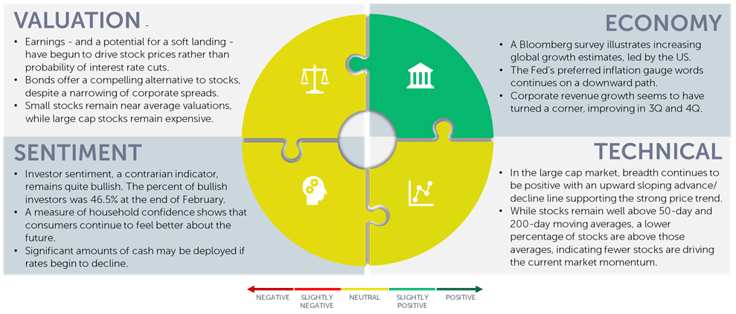

Our Navigator framework informs our outlook.

March 2024 Navigator Outlook

Economy: Growth estimates are increasing – a survey of Bloomberg economists increased global growth projections for 2024 and 2025; the US growth estimate has been upgraded by .6% in 2024. Inflation progressed on its downward trend as core PCE dropped to 2.8% YOY. Corporate revenue growth bottomed out in the second quarter, increasing to 2.4% in 3Q and 4% in 4Q 2023.

Technicals: The technical picture presents both positives and negatives. On the positive side, the S&P is in a strong up-trend and the NYSE Advance/Decline line has turned positive, indicating a broad market advance. On the negative side, a declining number of stocks are trading above their 50-day and 200-day moving averages. This indicates that while the gains are broad, momentum is being driven by fewer stocks.

Sentiment: Investor sentiment, a contrarian indicator, has been quite bullish since last summer. The current situation is in contrast to 2022, when a long period of bearishness gave way to strong returns; a lengthening period of bullishness today sets the stage for increased volatility and likelihood of losses in the coming months. The Conference Board Consumer confidence survey remains positive; this month we note that consumer expectations for their financial situation are improving. Additionally, significant cash remains on the sideline and may move into riskier assets if and when rates drop.

Valuation: Rate cut expectations have drove stock during 2023, but there has been a divergence in 2024; despite a reduction in the expected pace and timing of rate cuts, stocks have soared in 2024; this is due do solid growth and estimates for strong earnings in 2024. While stocks remain expensive, bonds provide an attractive yield relative to the earnings yield of stocks. Corporate and high yield spreads have narrowed, but absolute yields remain attractive. Small cap stocks trade at valuation levels close to their long-term averages, making them a compelling alternative to large cap stocks.

Outlook and Recommendations:

“In these matters the only certainty is that nothing is certain” - Pliny the Elder

The market has decided that we’ll have a soft landing. Let’s address the three economic scenarios and what factors might lead to each:

- Soft landing: A slowdown without a recession may, indeed, come to pass; economic growth estimates are being revised upwards, manufacturing activity is expanding, and the consumer is strong. Inflation is trending towards the Fed’s target of 2% - 2.5%. This appears to be a sensible base case at the moment.

- Hard landing: Recessions tend to happen after a fed rate-hiking cycle. This time around the banking sector appears weak due to unrealized losses on bank balance sheets, and potential write-downs of commercial property loans. Indicators of weakness in consumer credit are increasing. A credit crisis or increase in unemployment could put the expansion in peril.

- Growth ("No landing"): The AI boom could be a catalyst for increased growth, profitability and productivity. All these could lead to a new bull market led by US technological superiority. If this scenario plays out, we may be in the first inning of a wave that may lift all boats for several years.

In times of uncertainty the key is to think in terms of probabilities, focusing on avoiding bad outcomes if you are wrong.

Portfolio positioning

“By failing to prepare, you are preparing to fail.” ― Benjamin Franklin

Our portfolios are exposed to assets that prepare us for each scenario. Here are some examples:

- We have maintained our slightly overweight allocation to stocks, focused on large cap and mid cap growth shares which will benefit from a soft landing or growth scenario.

- We have shifted some of our mid cap allocation to small cap stocks, which should benefit portfolios in either a soft landing or growth scenario.

- We have maintained an allocation to high yield bonds. If growth resumes, corporations should be better able to support their corporate obligations.

- To protect against a downturn, we have maintained a diversified portfolio structure with flexibility to take advantage of market losses in a hard landing.

- In our alternatives portfolio we maintain allocations to a variety of strategies that offer diversification and downside protection.

With so much uncertainty about the economic scenario, it pays to be prepared for all potential outcomes. Our portfolios remain positioned to profit from a soft landing – the market’s base case - and offer some level of defense of a hard landing, while participating in the upside of a potential new bull market.

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00677