February 5, 2024 •Nathan Willis

Hold that thought

The progress of the economy in January threw cold water on the market’s hopes for interest rate declines. Much of the data surprised to the upside:

- Strong retail sales, low unemployment and strong wage gains affirmed the strength of the consumer.

- The initial estimate for fourth quarter GDP was 3.3%, well above the 2% estimate. This has led to increased estimates for 2024 and 2025 growth.

- The Fed’s preferred measure of inflation, core PCE, remains stubbornly high despite modest declines. Energy and supply chain issues pose upside risk.

The Fed kept rates steady at its January meeting. The normally mundane press release contained two significant changes:

- A prescient removal of this comment “…the US banking system is sound and resilient”. NY community Bancorp – the bank that took over much of Signature Bank during the banking crisis last march - dropped 40% after announcing significant losses related to commercial real estate. The stark loss is notable given less than a year has passed since the rescue.

- Removal of reference to further tightening was notable given the strong economic data and stubborn inflationary pressures.

These changes was viewed positively by the market, for a few minutes at least. However, Governor Powell downplayed expectations for rate cuts at his press conference following the meeting, noting the Fed would be “data-dependent”. This has caused the market to push expectations for rate cuts further out in 2024.

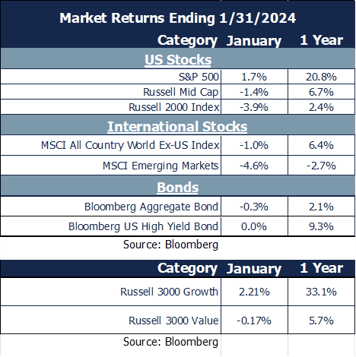

January Market Review

Markets digested changing expectations for the economy and the path of interest rates:

- Interest rates rose, causing modest losses for the broad bond market. High Yield bonds managed to remain flat.

- Large stocks rose 1.7%, leaving behind smaller cap and international stocks, all of which posted losses during the month.

- Small cap stocks were the worst domestic performer. Expectations for rate cuts that bolstered their returns in the fourth quarter were unwound, causing losses.

- Emerging markets suffered as questions continued about China’s economy.

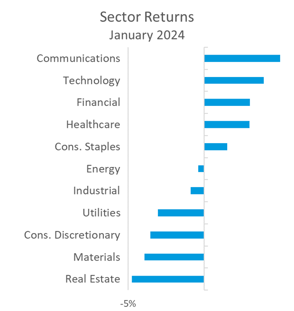

Sector movements returned to 2023 form.

- Technology and Communications Services, the two sectors containing the “Mega Cap 7” dominant stocks, led the way in January, repeating their dominance from 2023.

- Cyclical sectors, such as Real Estate and Consumer Discretionary, pulled back as the Fed put interest rate cuts on ice.

- Financials scored positive returns, despite increasing levels of concern about unrealized losses in commercial real estate loans.

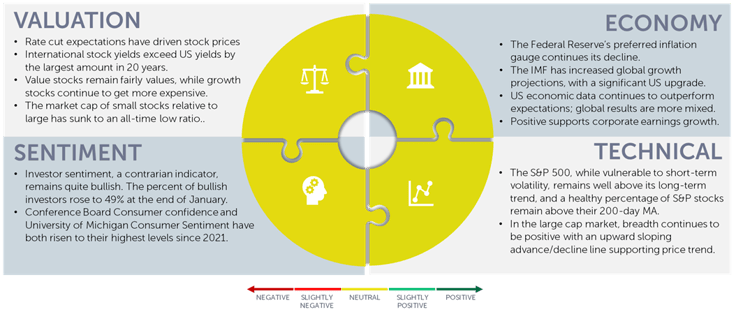

Our Navigator framework will inform expectations for 2024.

February 2024 Navigator Outlook

Economy: Inflation is slowly declining towards the Fed’s 2% - 2.5% target, but some inflationary pressures remain. The IMF, and others, have increased global growth projections for 2024 and 2025. The US received the most significant upgrade in growth estimate amongst developed economies. US data continues to outperform expectations, but non-US returns are more muted relative to projections. This positive economic data is supportive of strong profit growth in 2024.

Technicals: Despite being vulnerable to short-term volatility, the S&P 500 remains well above its long-term trend, with more than half of stocks in a positive trend as well. The number of advancing stocks divided by declining stocks remains strong and is supportive of the current positive price trend.

Sentiment: Investor sentiment, a contrarian indicator, remains quite bullish. While lower than the mid-December highs, the percent of bullish investors rose to 49% at the end of January. Both the Conference Board Consumer confidence and University of Michigan Consumer Sentiment have risen to their highest levels since 2021.

Valuation: Rate cut expectations have driven stock prices over the last several months as the market has processed the end of the rate-hiking cycle and eventual monetary easing. The S&P 500 remains expensive: International stock dividends exceeds S&P 500 dividends by the largest amount in 20 years. While growth stocks remain expensive, value stocks remain near average valuations and the market value of small-cap indices remains near all-time lows relative to the value of the S&P 500. Bonds, meanwhile, provide an attractive yield relative to recent history.

Outlook and Recommendations: “Dualing” Markets, Dueling Narratives

Dualism, a philosophical view which holds that the mental and physical are distinct and separable, resembles the market over the last year. Artificial intelligence innovations—deemed ethereal, celestial, and otherworldly —have driven returns meaningfully. The companies profiting from the mundane physical world and everyday business are, perhaps, in danger of being not only left behind economically but also co-opted by AI hype in the minds of investors.

The investment thesis of artificial intelligence echoes that of the late 1990s tech bubble: we’re not exactly sure how to value all the companies involved – or what how they’ll even make money from AI - but we’re pretty sure there are big opportunities afoot. There are also significant risks given recent stellar returns.

The evolving economy paired with potential game-changing technological innovation presents us with multiple narratives that are dueling for attention, with significant investment implications:

- Soft landing: Inflation is going to settle down without the economy experiencing a recession (the Federal Reserve’s assertion), and the Fed can start lowering interest rates. The fault in this narrative – at least the certainty its assertion – is this: we are coming off of a once in a life-time pandemic, with a once in a lifetime fiscal and monetary response, which has followed a 15-year, unprecedented money printing experiment to save us from the 2008 global financial crisis (one which the Fed assured us wouldn’t happen). This is the market’s base case, but it is not by any means certain. The Fed’s confidence reminds of the first cinematic portrayal of artificial intelligence: HAL9000: I know I've made some very poor decisions recently, but I can give you my complete assurance that my work will be back to normal. I've still got the greatest enthusiasm and confidence in the mission. And I want to help you.[1]

- Hard landing: The Fed has made a major policy error by raising rates too much and will drive us into recession. The sharp rise in interest rates will decimate the financial system leading to certain recession. Recent banking failures highlight the noteworthy risk of a hard landing.

- No landing: The US consumer is resilient; AI will power the economy to greater heights. Alternatively, the cousin of the ‘no landing’ scenario is that we’re in the midst of a rolling recession. Tech and the consumer sectors have already experienced a recession, and their recovery will keep things afloat while real estate, financial and other sectors work through their recessions. The strength of the consumer lends support to this view and the employment picture appears solid enough to suggest we may move past potential risks.

Evidence supporting each scenario is complicated by unprecedented nature of the various fiscal and monetary stimulus of the last decade and a half. We really don’t have a great read on how they will all play out. In times of uncertainty the key is to think in probabilities and focus on avoiding bad outcomes if you are wrong.

Portfolio positioning

One of the core tenets of our process is that we are focused on the long-term. At the same time, we are presented with risks and opportunities that leads to a couple of portfolio recommendations:

- Focus on high quality stocks that are fairly valued. Fairly valued holdings offer higher likelihood of solid long-term returns than stocks with high valuations.

- Think long-term. Remain focused on your plan and be sure your portfolio is moving you towards your plan, rather than trying to bet on one specific scenario in the short term.

- Remember bonds: bond yields are higher than the earnings yield from stocks and offer a compelling balance of risk and reward. Cash yields are likely to decline as inflation drops; consider putting cash to work in the markets.

- Consider diversification into alternative strategies. While bond yields are compelling, they have not provided a lot of diversification to stocks in the last couple of years. Consider strategies that hedge risk or those which may act differently than the rest of your portfolio.

With so much uncertainty about the outlook for 2024, we remind investors to remain disciplined, and diversified. Our portfolios remain positioned to profit from growth and offer some level of defense in a downturn. If you need a checkup to be sure your portfolio is on target, or if it is not clear why your portfolio is structured the way it is, reach out to your advisor.

[1] Source: 2001, A Space Odyssey, Directed by Stanley Kubrick, Metro-Goldwyn-Mayer, 1968

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00662