March 6, 2023 •Nathan Willis

Reality Check

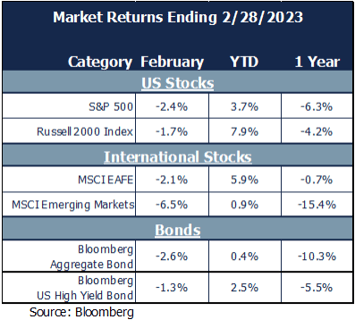

Markets retreated this month after January’s strong returns.

- Minutes of the January 31 – February 1 Fed meeting reflected expectations that the Fed would keep rates high for the remainder of 2023.

- Markets had been expecting rate cuts would commence sometime in 2023.

- The adjustment to higher rates caused both stocks to sell off alongside bonds.

- Inflation data came in stronger throughout the month and earnings estimates continued to decline.

February Market Review

The S&P 500 lost 2.4% during February, giving back 1/3 of January’s stellar returns. International stocks underperformed:

- Developed international stocks finished down 2.1% while emerging markets lost 6.5%.

US bonds also lost ground: - The Bloomberg Barclay’s Aggregate lost 2.6% while high yield bonds lost 1.3%.

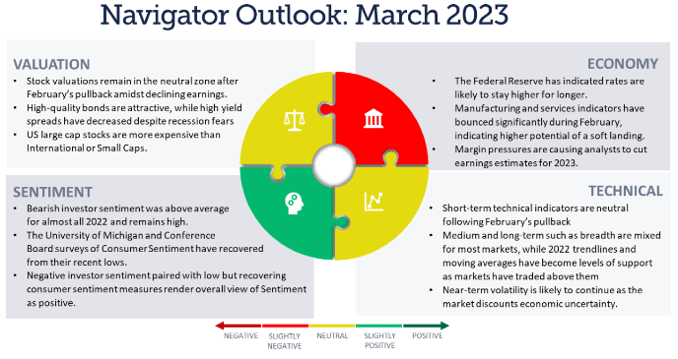

We follow our Navigator process to maintain discipline and perspective. Let’s review what it is telling us.

Navigator Process

Valuation: S&P 500 valuations have pulled back to 18 times earnings, close to the 25-year average. International and small caps remain less expensive than US large cap stocks, and value stocks remain less expensive than growth-oriented names. Stock valuations are neutral when compared with bonds; the rise in yields over the last two years has made bonds are more attractive, relative to stocks, than they have been in quite some time. Fixed income spreads shrunk during February, indicating solid returns are available in the bond market without taking excessive risk.

Economy:The ISM (Institute for Supply Management) survey of new orders rebounded to 47 from 42.5 in January. While the two other times this measure has been lower in the last 20 years were during the pandemic and the Global Financial Crisis, the rebound in this leading indicator provides reason for optimism. The Federal Reserve remains focused on fighting inflation by slowing the economy.

Economic indicators are negative; the caveat to this negativity is that a recession is the consensus on Wall Street. We are not predicting that we avoid one, but one data point that we have highlighted in the past is high yield spreads, which remain low.

Investors in these bonds are not requiring the extra income investors usually require when a recession, and corporate bond defaults, are on the horizon.

Technicals: Technical indicators are neutral overall. Markets seem to be finding support at the 200 day moving averages and have broken through the 2022 downtrends—resistance levels that, now they have been broken, have become support levels. Market breadth has turned negative for almost all markets, consistent with the downturn in stocks.

Sentiment: Investor sentiment remains the bright spot; it has been negative most of the time since the summer. We view investor sentiment as a contrary indicator and, combined with recovering consumer sentiment, as a positive for the markets.

Outlook and recommendations: winning a tug of war by dropping the rope.

The economic data got stronger during February, affirming the need for the Fed to raise rates higher and keep them there longer than the market has been expecting. On the other hand, the expected downturn at the Fed’s hand be just a bump in the road to the post-pandemic stock market and economic recovery.

The technical picture and investor psychology contain cause for optimism. Investors are bearish, a positive sign, and stock markets have broken the downward-sloping trendlines of 2022. They currently trade above several technical levels, such as the 200-day moving average. The stock market is a leading indicator, and it may be telling us things will work out just fine. High yield bond spreads remain narrow, indicating the bond market is not worried about a recession either.

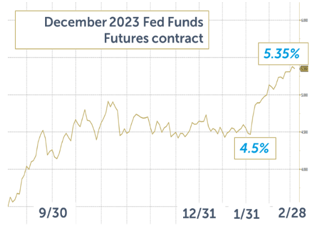

There are headwinds to the optimistic view. The Fed has been steadfast in its commitment to taming inflation, and the market is taking note: After 4 months of calm, the December 2023 Fed Funds futures contract shot up from 4.5% in January to 5.35% at the end of February. This was a significant shift up in expectations as the bond market recognized the Fed’s commitment. Valuation risks for stocks are highlighted by the fact that when markets retreat from peak to average valuation levels - as they have done over the last year and a half - they overshoot to the downside more often than they recover.

There are headwinds to the optimistic view. The Fed has been steadfast in its commitment to taming inflation, and the market is taking note: After 4 months of calm, the December 2023 Fed Funds futures contract shot up from 4.5% in January to 5.35% at the end of February. This was a significant shift up in expectations as the bond market recognized the Fed’s commitment. Valuation risks for stocks are highlighted by the fact that when markets retreat from peak to average valuation levels - as they have done over the last year and a half - they overshoot to the downside more often than they recover.

As a parent of three young boys, I have been given wise advice: to win a tug of war with your kids, sometimes you need to “drop the rope”, leaving the conflict alone. Rather than tug strongly on one side of the stock market debate, it makes sense to acknowledge the uncertainty. We recommend investors:

- Acknowledge the volatility: Don’t be surprised by it; use it to your advantage.

- Consider alternative investments: Strategies with lower correlation may protect your portfolio from downside and may protect you from making a poor decision to sell when stocks are down.

- Remain invested: OneAscent portfolios are fully invested. Our tactical sleeve is evenly allocated between stock and bond investments, giving us the ability to add risk on a selloff but to capture returns if the market trades higher.

- Consider active tax management: Volatility offers opportunities to realize “tax-alpha” to improve your overall financial returns. Talk to your advisor to see where the opportunities lie.

Maintain discipline: Above all, maintain discipline and stick with your plan. OneAscent portfolios remain fully invested at our target allocations, despite risks to the upside and downside.

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00203