January 4, 2024 •Nathan Willis

Soft landings and the Mona Lisa

The Mona Lisa is valuable for its rarity and history as well as for its beauty. And it may never have been completed![1]There are parallels in today’s investment markets.

While November highlighted the changing dynamics between the stock and bond markets, Federal Reserve governor Powell made it clear that – in the Fed’s mind – their work is finished; the elusive and rare soft landing is coming our way in 2024[2]

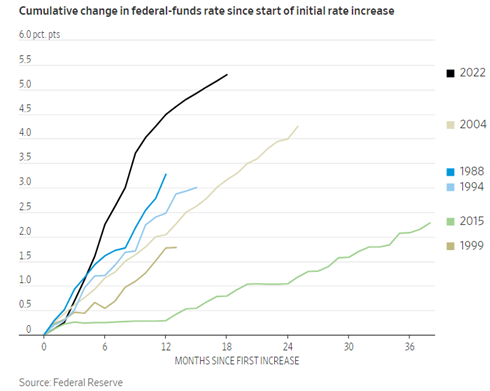

Soft landings, while not as rare as the Mona Lisa, are scarce – the Fed only engineered a soft landing after two of the last nine tightening cycles. This chart illustrates the difficulty; it was the harshest tightening cycle on record. Meanwhile COVID stimulus programs have ended, and the Fed is attempting a delicate exit from the Post-GFC (’08 Global Financial Crisis) Quantitative Easing experiment.

Let’s review December market returns, our outlook, and portfolio positioning.

December Market Review

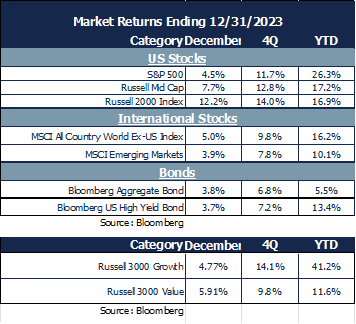

Markets continued to soar:

- Interest rates dropped across the yield curve – The ten-year treasury dropped from 4.3% to 3.8%, resulting in better than 3% bond returns.

- Large stocks rose 4.5%, while, importantly, market returns broadened beyond the 2023 leaders, carrying mid and small caps even higher. International stocks came along for the ride as well.

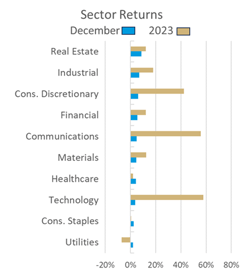

Interest rate movements drove sector returns again:

- After erasing YTD losses in November, Real Estate gained a further 9% for the month.

- Cyclical sectors such as industrials, consumer discretionary and financials performed well on optimism for a soft landing.

- What sticks out, though, is that returns were found outside the three sectors that contain the “magnificent 7” stocks (tech, communications and Consumer discretionary). Increasing breadth may support further stock gains.

Our Navigator framework will inform expectations for 2024.

January 2024 Navigator Outlook

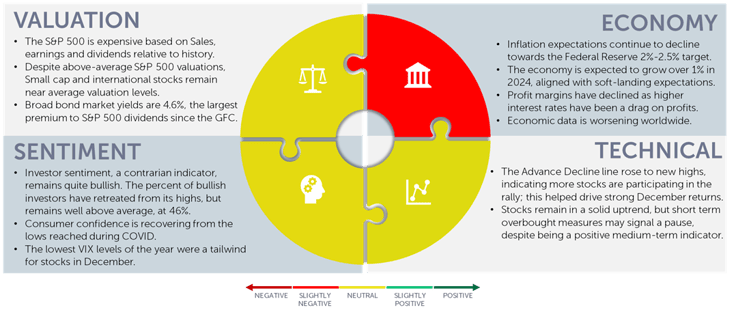

Economy: Inflation expectations – which affect actual inflation - continue to decline towards the Federal Reserve target of 2 – 2.5%. The economy is expected to grow over 1% in 2024, aligned with expectations of a soft-landing. Profit margins have declined in 2023, as in 2022, as higher interest rates have been a drag on profits. Across global markets, the economic data is worsening in a coordinated manner.

Technicals: The Advance Decline line rose to new highs, indicating more stocks are participating in the rally; this helped drive strong December returns. Stocks remain in a solid uptrend, well above the 200-day moving average, but short-term overbought measures such as the RSI (Relative Strength Index) may signal a pause despite being a positive indicator for medium-term returns.

Sentiment: Investor sentiment, a contrarian indicator, remains quite bullish. The percentage of bullish investors has retreated from its highs, but remains well above average, at 46% bulls. Consumer confidence is recovering from the lows reached during COVID, and this is reflected in the financial markets as the VIX, the so-called ‘volatility index’ declined to its lowest level of the year in December. Declining volatility has been a strong tailwind for the stock market in 2023.

Valuation: The S&am;P 500 remains expensive, relative to history, based on multiple measures: price/sales, price/earnings and dividend yields. Small cap and international stocks, however, remain near average valuation levels. The Bloomberg Aggregate Bond Index yield is 4.6%, the largest premium to S&P 500 dividends since the GFC.

Outlook and Recommendations: Mission accomplished

"Nature never breaks her own laws." – Leonardo da Vinci

The comparison of the Mona Lisa to the markets is apt: it would indeed be a rare event for the Fed to achieve a soft landing; especially so given the unprecedented nature of our economic system today, including:

- We are living through the end of the harshest hiking cycle in Federal Reserve history in terms of speed and amount of increase.

- COVID stimulus programs are finished; the resumption of student loan payments in 2023 marks the end of pandemic assistance programs.[3]

- The Federal Reserve is shrinking its balance sheet again. Unwinding the unprecedented stimulus – created to stabilize the economy during the 2008 Global Financial Crisis - is likely a headwind to economic growth.

Another historical comparison may fit the current situation: 20 years ago, George W. Bush gave the infamous “mission accomplished” speech, announcing the end of major combat operations in the Gulf War. The analogy for today comes from within the President’s speech that day: "We have difficult work to do…” and “…we have seen the turning of the tide."

Despite justifiable optimism over a potential soft landing, the work to accomplish one may be far more difficult than the market perceives. Two bad outcomes may happen instead of a soft landing: a ‘hard landing’ (recession), or an acceleration of inflation, with further rate hikes. What is an investor to do in the wake of such uncertainty?

Optimism, pessimism, or both?

"An optimist thinks that this is the best possible world. A pessimist fears that this is true." – Robert Oppenheimer

This quote sounds like risk management, which is what we recommend.

Economic data is inconsistent – Leading indicators and credit metrics indicate a slowdown, but strong labor markets and consumer spending indicate remaining strength in the economy. This leads to a couple of portfolio recommendations:

- Don’t bet too much on one outcome. Look for assets that have the potential to perform well in various scenarios.

- Diversify. Something you are doing now is probably not going to work right; this is the nature of uncertainty. Diversification tends to lessen the negative impact of your reactions when things don’t work out according to your plan.

- Think long-term. A key factor in long-term returns is valuation: the price you pay today has very little to do with next year’s returns, but a whole lot to do with the next decade’s return. Pay attention to the price you pay and what it means for long-term returns.

- Don’t chase what worked last year. Technology stocks – specifically the “Magnificent 7” drove markets in 2023.

Likewise, Technology stocks were on a tear in 1998 and 1999, only to lose all of those gains from 2000 through 2002.

You might want to consider areas beyond what is currently fashionable.

Hopefully these principles will help you manage through the uncertainties of 2024. While we are open to optimistic market scenarios – with some healthy skepticism - the principles above translate into some specific portfolio exposures.

- Bonds offer attractive yields at today’s levels. This higher yield offers a cushion to both rising rates and, for corporate bonds higher yields offer a cushion against downgrades or defaults that may occur during a recession.

- Diversification is a sound strategy – particularly when it hasn’t worked well. Alternative strategies have lagged the US Stock market; 2024 may reward diversification and non-correlated strategies.

- Think long-term. The most significant driver of long-term returns is the price you pay. We see attractive values in International, Small, and Mid-cap stocks.

Finally, I leave you with one more piece of advice. Stop listening to what other people think – including us! Rather, pay attention to why we think what we think. We put a lot of thought into how we build portfolios; If it is not clear why your portfolio is structured the way it is, reach out to your advisor. We are happy to explain the rationale for portfolio decisions we are making.

Finally, and as always, stick with your plan. If you are worried, consult with your advisors to make sure you are on track. We wish you a wonderful Christmas season and a happy 2024.

We wish you a wonderful and prosperous 2024.

[1] Source: The Guardian Da Vinci 'paralysis left Mona Lisa unfinished' | World news | The Guardian

[2] Source: Wall Street Journal, Federal Reserve Powell’s Pivot Sows Confusion Over When and How Fast Fed Will Cut - WSJ

[3] Source: CNN Pandemic-era relief program benefits are ending for some people | CNN Politics

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00573