August 5, 2024 •Nathan Willis

July Review – Cooler Inflation Triggers a Massive Rotation into Small Cap Stocks

On July 10, the Bureau of Labor Statistics reported that consumer inflation came in below expectations for the month of June. This continued the movement towards the Fed’s target and the increased likelihood of rate cuts triggered a sharp rotation out of 2024’s winners – primarily tech stocks - into small cap stocks which are considered particularly sensitive to interest rates.

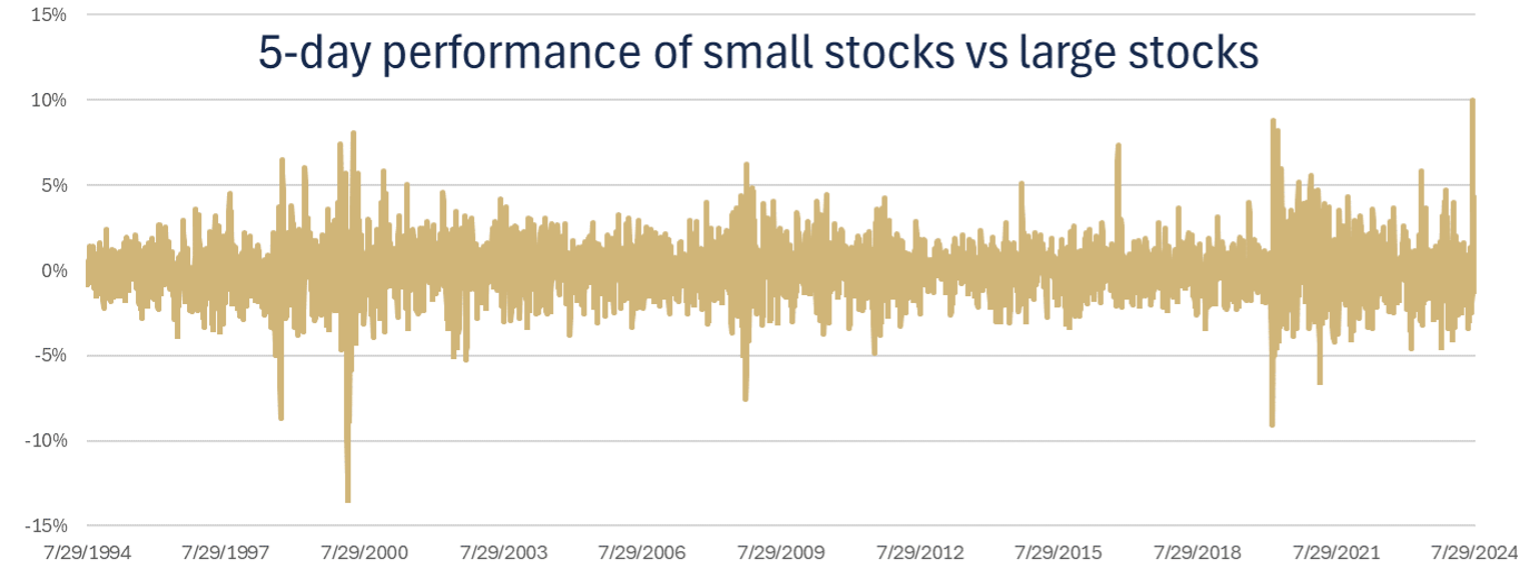

The chart to the left shows the magnitude of the shift – over the next 5 days, small cap stocks outperformed large caps by 10% - the largest such streak on record.[1]

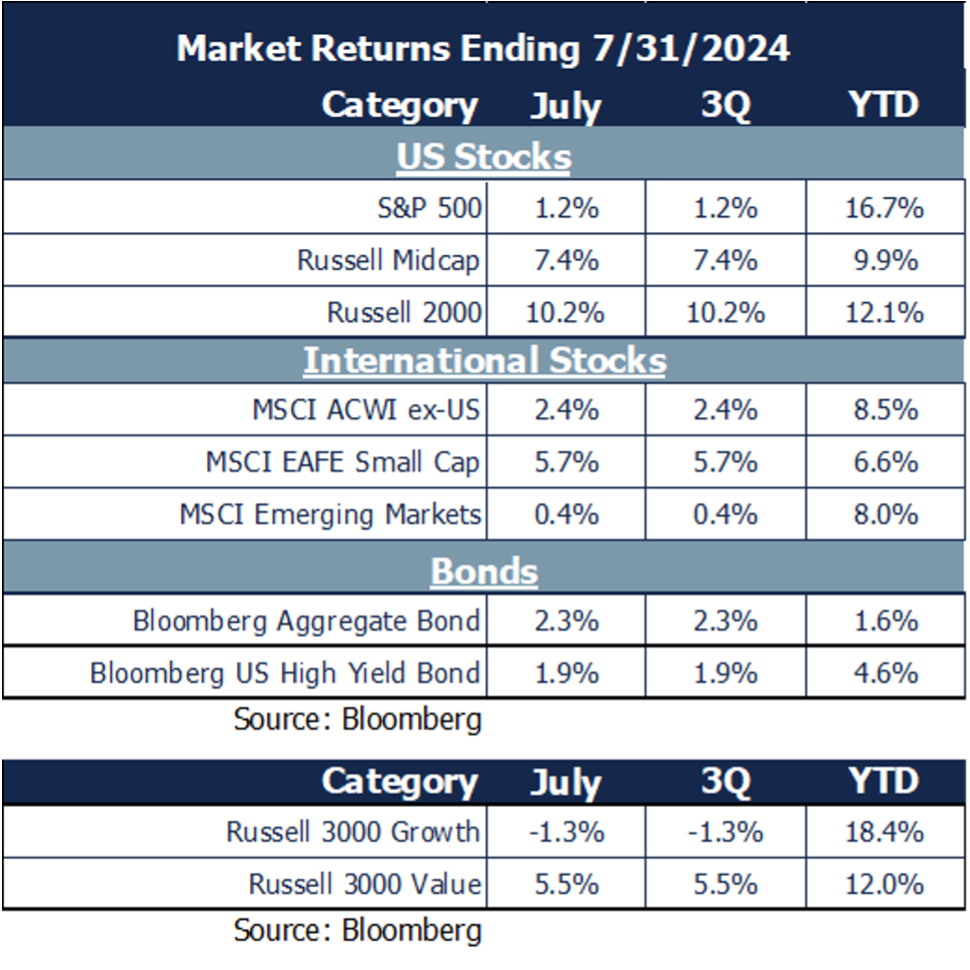

During the month of July, small cap stocks were up over 10% while the S&P 500 gained less than 1% and technology stocks lost 2%. We will talk about what this rotation means for the remainder of the year in the outlook section.

June Market Review

The rotation from large to small was not the only Highlight of July:

- Large cap stocks are up 16% for the year after managing a slight gain of 1.2%.

- International stocks joined small caps in outperforming the S&P 500, but emerging markets took a break from their recent strong performance.

- Value stocks roared back this month, but growth remains firmly ahead for the year.

- Bonds rallied on the soft inflation news and Fed Chair Powell’s dovish comments near the end of the month.

Stock sector movements reflected the slowing inflation and dovish Fed:

- Interest sensitive sectors – Real Estate, Utilities, and Financials – led the way as the market perceived that interest rate cuts are imminent. These sectors are expected to perform well during a period of declining rates.

- Technology and communications were the only sectors in the red for the month, giving up a small portion of their strong YTD gains.

- Consumer staples and discretionary stocks managed to score slight gains despite growing evidence of strains in consumer balance sheets.

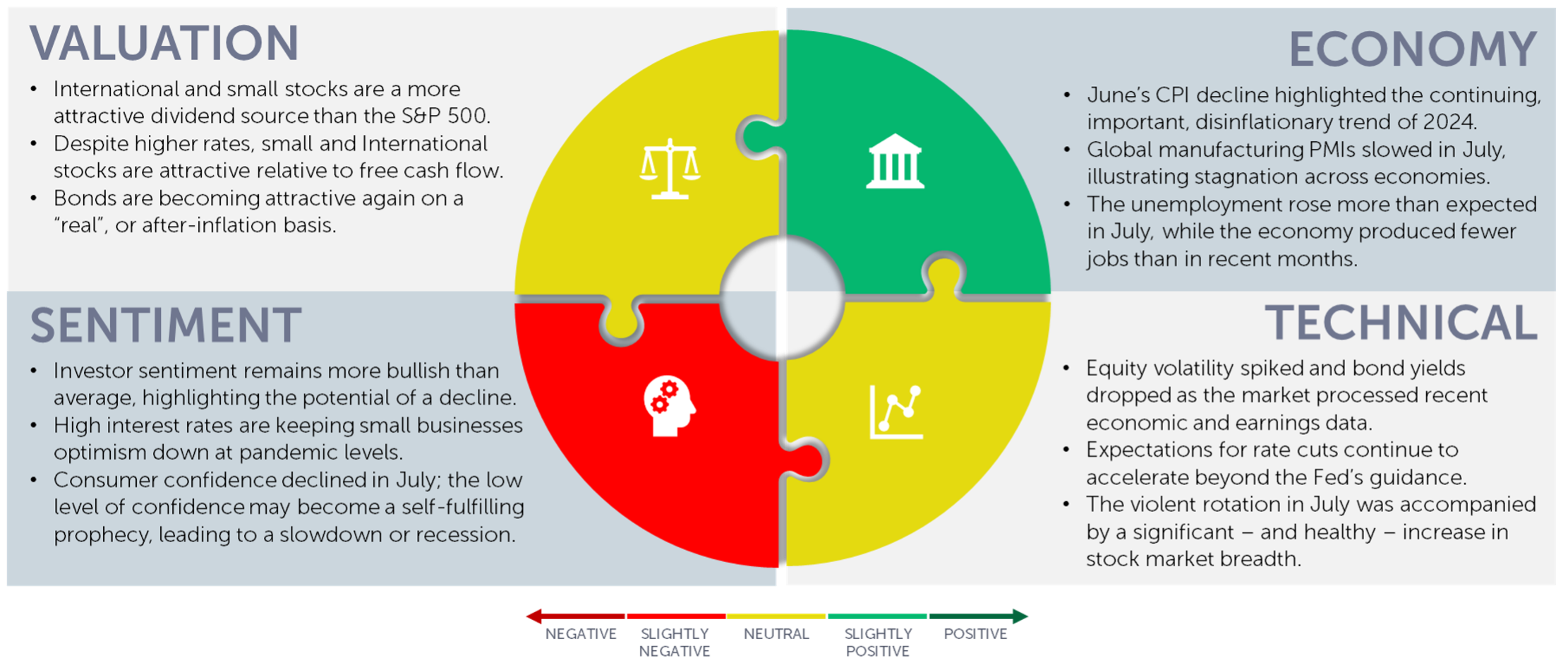

Our Navigator framework informs our outlook.

August 2024 Navigator Outlook

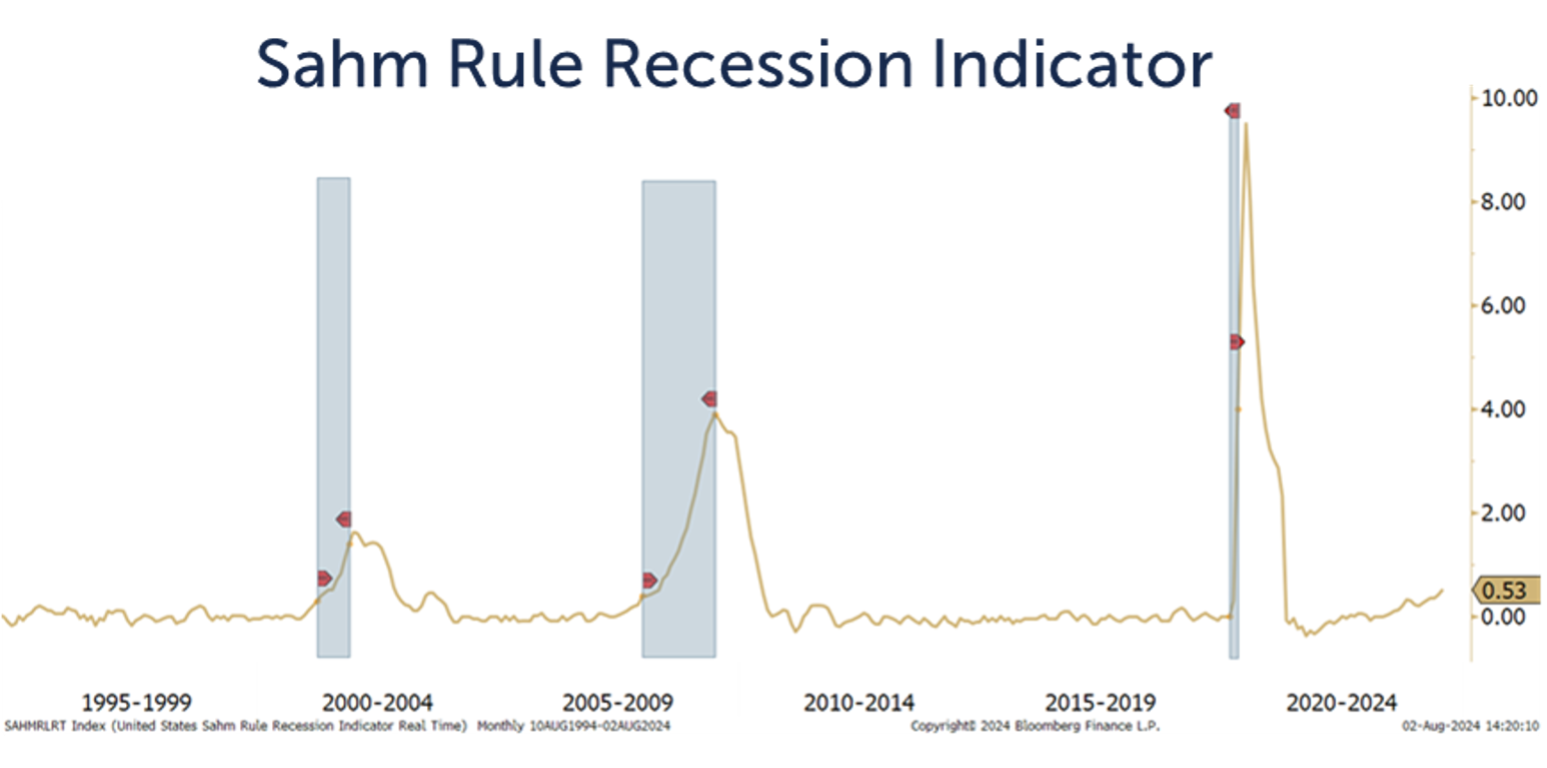

Economy: June’s lower CPI inflation report highlighted the continuation of 2024’s disinflationary trend. Global manufacturing PMI measures slowed in July, showing some signs of economic stagnation. July’s unemployment report showed a rise to 4.3% and triggered the “Sahm rule,” suggesting a recession may be imminent.[2]

Technicals: Equity volatility spiked, and bond yields dropped as the market processed weaker economic data and earnings reports. Expectations for rate cuts continue to accelerate beyond the Fed’s guidance, increasing market worries that the Fed may be behind the curve in preventing recession. July’s violent sector rotation was accompanied by a significant – and healthy – increase in stock market breadth.

Sentiment: Investor sentiment remains more bullish than average; this may lead to an increased risk of a decline. High interest rates are keeping small business optimism down at pandemic levels. Consumer confidence declined; the dour mood may become a self-fulfilling prophecy, leading to further slowdown or recession.

Valuation: International and small stocks are a more attractive source of dividend income than the S&P 500 and have increased their advantage in recent months. Despite higher interest rates, small and international stocks remain attractive relative to free cash flow. Bonds are becoming attractive again after accounting for inflation.

Outlook and Recommendations: Does Weak Data Expose a Weak Fed?

The risk that a soft landing would turn into a hard landing has always been greater than the market narrative would proclaim. That narrative was turned on its head in July as economic data deteriorated and several stocks with AI related theses missed earnings estimates. The July employment report was the icing on the cake; the economy produced fewer jobs than expected and the unemployment rate rose more than expected; in fact, the increase in the unemployment rate has triggered the “Sahm Rule” which has a perfect record of forecasting recessions. Recession is predicted when the unemployment rises to .5% higher than the average of the prior 12 months, as illustrated here (recessions in gray):

Increased recession risk caused the markets to aggressively price more rate cuts; the market has also re-evaluated the sharp rotation into small cap stocks during July. The worry is that the Fed is “behind the curve," meaning they have already missed the opportunity to avoid recession by cutting rates. We continue to believe that a recession is a distinct possibility and have taken steps to position appropriately.

Given the lunacy that characterizes this presidential race, a comment on the election is warranted. More democrats than republicans are up for re-election in the Senate while several blue-state republicans are retiring in the house.[3] This leads to a high probability of split government - the market’s preferred scenario - whomever wins the presidency. While there are well-known policy differences between the two, the market is not likely to perform substantially better under either candidate’s administration.

Portfolio Positioning

Amidst these risks we see numerous opportunities and are positioned accordingly:

- We reduced our growth exposure and are focused on high quality stocks.

- We reduced our high-yield bond allocation by shifting to investment grade corporate bonds; these bonds should fare better should recession occur.

- We shifted out of short-term bonds into intermediate duration corporate bonds in our tactical portfolio sleeve; this will allow us to capture more total return, including a higher level of income, if short-term rates decline.

- We have also shifted from mid-cap stocks to emerging markets in our tactical sleeve; emerging economies are faring better than developed, and emerging market corporate earnings are showing improvement.

We have suggested for some time that the high valuations that exist in the stock market create a situation where volatility may spike, and that is playing out. Short-term losses are a fact of investing life; we are prepared to take advantage of the opportunities presented by this volatility. We encourage investors to remain prepared, calm, and fully invested, during both good times and challenging markets.

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Bloomberg, OneAscent Investment Solutions

[2] Source: Bloomberg, Sahm Consulting Sahm Consulting (claudiasahm.com)

[3] Source: Ballotpedia.org Ballotpedia, 270towin 270toWin - 2024 Presidential Election Interactive Map

OAI00912