September 5, 2023 •Nathan Willis

Great Expectations

“Ask no questions, and you'll be told no lies.”

― Charles Dickens, Great Expectations

Strong economic data and stock returns this summer have led investors to have high expectations. This month we will ask questions about growth, inflation, earnings, and investment returns:

- Is the economy on a solid foundation with accelerating growth?

- Is inflation falling to the Fed’s target, and have they finished raising rates?

- Are estimates of company earnings appropriate?

- Do stock and bond valuations allow for acceptable returns going forward?

The answers appear to be “yes” to all four questions. GDP growth estimates are soaring, inflation is coming down more than expected, earnings are recovering, and – outside of US large cap stocks – valuations suggest decent long-term returns.

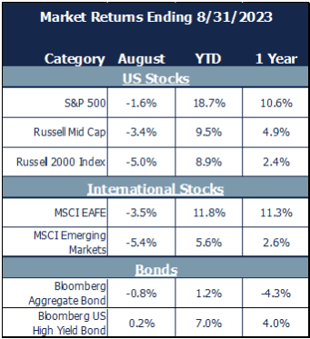

August Market Review

Stocks floundered to close out the summer:

- Large stocks ended down 1.6%; Mid, small, and international stocks all experienced greater losses as investors’ appetite for risk declined.

- Quality bonds dropped as growth accelerated, easing recession fears and bringing inflation to the front and center.

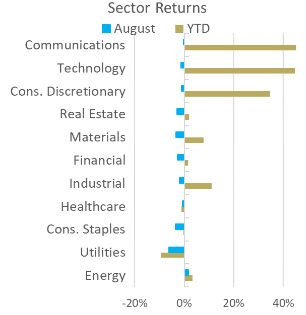

- All sectors except energy lost money; utilities – the most ‘bond-like’ – fell the most.

- Value and growth showed similar losses.

High expectations created by the summer’s economic performance (and reflected in asset valuations) have buoyed sentiment and the market’s technical backdrop. Let’s review our Navigator framework to develop our own expectations.

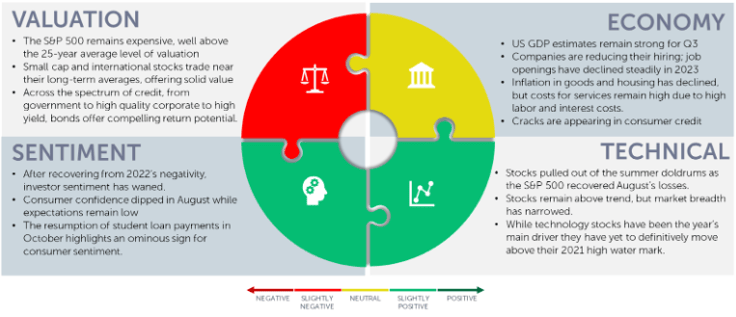

September 2023 Navigator Outlook

Economy: The month of August saw better than expected consumer data; employment and retail sales were very strong. Despite modest manufacturing data, GDP estimates remain high. Inflation remains low, though the stickiness of inflation in the services sector persists. Potential stress is emerging in the consumer sector; credit cards and auto loans are showing some stress among lower quality borrowers.

Technicals: Stocks pulled out of the summer doldrums by breaking back above short-term moving averages and above August’s downtrend. While the market’s momentum remains positive, breadth remains weak with fewer stocks participating in the rally. Technology stocks, the year’s driver, have yet to definitively break above their high-water mark from 2021.

Sentiment: Investor sentiment recovered from a long stretch in negative territory but waned in August. Consumer sentiment has also recovered from the historic lows of 2022, and the expectations component is still low. One cloud on the sentiment horizon is student loan payments, scheduled to resume in October.

Valuation: The S&P 500 remains expensive relative to bonds and to other stock markets. International and small cap stocks remain at a significant valuation discount to the S&P 500, trading more in-line with their long-term averages. Bonds remain attractive across the spectrum of credit risk.

Outlook and recommendations: Expectations and reality

“Take nothing on its looks; take everything on evidence. There's no better rule.”

― Charles Dickens, Great Expectations

Sentiment and market technicals are supportive of stocks in the near term. As we evaluate expectations in light of the evidence we just reviewed, we can draw longer term conclusions for our portfolios:

- The economy has shown surprising strength. However, there are some excellent reasons to be cautious. Bank lending and corporate hiring have both been slowing. Auto and credit card delinquencies are increasing, a situation likely to worsen unemployment ticks higher.

- Inflation has been coming down, no doubt. However, the Fed’s “supercore” inflation measure, which excludes housing, remains sticky. Labor costs and interest rates play a big factor in the service sectors, keeping this measure higher. Therefore the Fed’s commitment to bringing inflation down is likely to result in a worsening employment situation.

- Earnings have remained solid in the US while remaining more subdued in the rest of the world. In fact, calendar year 2023 and 2024 earnings estimates have increased throughout the month of August, fewer companies are citing the word “recession” on earnings calls, and profit margins have stabilized.[1]

- US large cap valuations remain extended; the S&P is overvalued by most measures.[2] Small and international stocks, however, present compelling long-term value. These markets are trading close to their long-term average valuations. Bonds offer compelling yields across the credit spectrum.

While the data seems to point to an increasing likelihood of a soft landing, we need to be prepared for all scenarios.

Our advice to investors:

- Maintain discipline. Do not try to time the market. If you are under or over-invested, determine your destination and follow your plan.

- Remain diversified. In particular, bonds offer return potential in a way they haven’t for some years. Many stock markets present sound opportunities.

- Consider alternative investments. Strategies with low correlation to the overall markets meet a crucial need in many portfolios.

- Remain invested. Taking these points to heart will help you stay the course.

A solid look at the evidence gives us optimism for the long-term. Don’t be surprised, though, by volatility, as high expectations leave little room for error. The reality is that September performance, on average, is negative. When the index is up at least 10% through August – as it is this year – it averages a slight gain.[3]Long-term investors are wise to ignore the short-term noise this month.

[1] Source: FactSet

[2] Source: JPMorgan Guide to the Markets

[3] Source: Barrons What's Next for the S&P 500, According to History (barrons.com)

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

OAI00419