April 2, 2024 •Nathan Willis

March review – What are we waiting for?

Most of us are waiting. We're waiting for something interesting to happen. And I think we're going to wait forever if we don't do something more interesting with our lives.

- Donald Miller

This quote offers wisdom for our investment portfolios; we can do a lot of interesting things while waiting for the next recession or bear market. In fact, Federal Reserve Governor Powell told us to stop waiting for a recession. Given the steady decline in inflation, the Fed will likely cut rates sometime in 2024, keeping recession at bay.

The markets have been waiting for rate cuts to begin. These expectations drove returns during March.

Some are waiting for an imminent recession. Should they? More on that later.

March Market Review

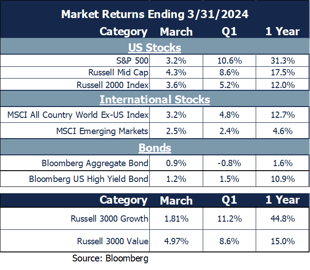

Markets rose broadly in March:

-

-

-

-

- Bonds gained with increased clarity on rate cuts. High Yield performed better than investment grade.

- Large stocks rose 3.2%, but small and mid-cap stocks performed even better.

- Value stocks outperformed growth.

-

-

-

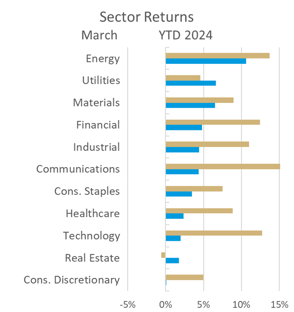

Stock sectors reflected rate cut expectations:

-

-

-

-

- Energy was the top performer as growth expectations accelerated.

- Utilities reacted positively to lower rates.

- Tech and the Consumer underperformed as Apple and Meta, respectively, continued their first quarter selloffs during March, reflecting a potential shift away from 2023’s dominant stocks.

-

-

-

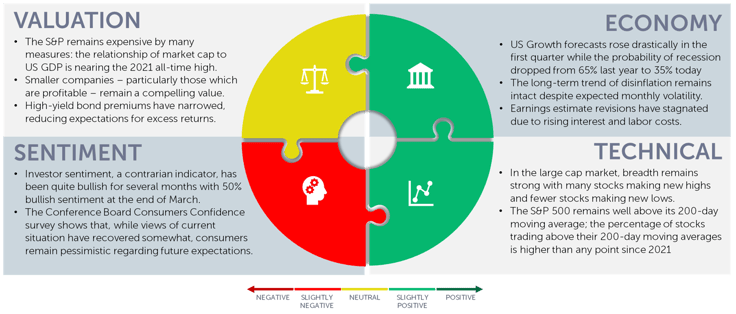

Our Navigator framework informs our outlook.

April 2024 Navigator Outlook

Economy: US Growth forecasts rose drastically in the first quarter while the probability of recession dropped from 65% during the summer of 2023 to 35% today[1]. The long-term trend of disinflation remains intact despite expected monthly volatility. Earnings estimate revisions for the full calendar year 2024 have stagnated, likely due to rising interest and labor costs.

Technicals: In the large cap market, breadth remains strong with many stocks making new highs and fewer stocks making new lows. The S&P 500 remains well above its 200-day moving average and the percentage of S&P 500 stocks trading above their respective 200-day moving averages is higher than any point since 2021.

Sentiment: Investor sentiment, a contrarian indicator, has been quite bullish for several months, registering 50% bullish sentiment in March. As bullish sentiment persists, the likelihood of a larger and/or longer pullback increases. The Conference Board Consumers Confidence survey shows that, while views of current situation have recovered somewhat, pessimism regarding future expectations persists.

Valuation: The S&P 500 remains expensive by many measures: the relationship of market cap to US GDP is nearing the 2021 all-time high. Smaller companies – particularly those which are profitable – remain a compelling value; the S&P 600, which includes a profitability component, has maintained attractive valuation while the Russell 2000 valuation has grown steadily over the last decade. High-yield bond premiums have narrowed, reducing expectations for excess returns.

Outlook and Recommendations: What we wait for, and what we do while waiting

“Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in corrections themselves.” - Peter Lynch

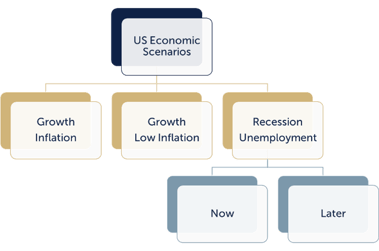

The question “what are we waiting for” is rhetorical. A framework for thinking ab out this is shown to the right; the market expects a soft landing – growth with low inflation.

out this is shown to the right; the market expects a soft landing – growth with low inflation.

But we know a recession will eventually happen. The question is really when, not if: will it be now (in 2024 as a result of the Fed raising rates too far, too fast) or later (as the economy goes through its normal ups and downs).

The answer to that question is not nearly as important as the answer to the question: “what should we do while we wait?”. Our goal is to build portfolios with potential to perform well across a range of scenarios. Most portfolios will do fine in a low growth, disinflationary environment, so we will focus on what we are doing to protect against inflation or recession:

- Growth and high inflation – A “no landing” scenario with high inflation would cause the Fed’s to raise rates instead of lower them, surprising most everyone.

- Recession with higher unemployment rate - The “hard landing” scenario would likely derail consumers, corporate profits, stock markets and the Fed.

Portfolio positioning

Our portfolios are exposed to assets that prepare us for each scenario; they are also built with a long-term horizon. One key principle of portfolio construction is that starting points matter. Two portfolio examples highlight our thinking:

- Over the last few quarters, we have reduced our allocations to growth-oriented stocks with higher valuations. We have added both mid cap and small cap value managers, lowering overall portfolio valuation. If inflation increases, these stocks are likely to suffer less P/E compression.[2] Their modest valuations provide a margin of safety that would benefit portfolios during recession.

- We have maintained an allocation to high yield bonds. Despite the fact that high yield spreads have declined relative to treasuries, they offer solid return expectations relative to stocks. High yield bonds are likely to perform better than the rest of the bond market in an inflationary environment.[3] Their higher current yields offer a buffer against increased defaults that would likely occur during a recession[4].

Reflecting from the quote that led off this note, there are things we can do that are far more interesting (and productive) than worrying about a recession; value stocks and high yield bonds are two assets that are likely to perform well ‘while we wait’ for the market’s hoped-for soft-landing, inflationary, or recessionary outcomes.

Recessions and bear markets happen regularly; the key to success is to avoid mistakes during periods of volatility by building robust portfolios. Our portfolios are likely to profit if we experience a soft landing – the market’s base case – but offer some defense against an inflationary environment or a recession. This allows investors to stay in the game during the inevitable challenging markets.

This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: Bloomberg Economics

[2] Source: Bloomberg. While high the p/e S&P 500 Technology Index lost 28% in 2022, the S&P 500 as a whole lost 18%, while value stocks, measured by the Russell 3000 Value Index, lost 8%.

[3] Source: From peak (8/7/2020) to trough (10/20/2022) the Bloomberg Barclays Aggregate Index lost 18.31%, while the Bloomberg US Corporate High Yield Index lost 4.48%. During 2023, the Aggregate gained 5.53% while the High Yield Index gained 13.45%

[4] Source: One March 31, the ICE BofA US High Yield Index Effective Yield was 7.5%, ICE BofA US High Yield Index Effective Yield (BAMLH0A0HYM2EY) | FRED | St. Louis Fed (stlouisfed.org) S&P Global is forecasting high yield defaults to rise to 4.75% in 2024 Elevated Interest Rates Are Pushing U.S. Corporates Into Default (forbes.com)

OAI00690